ECB - Virtual currency schemes Review

ECB - Virtual currency schemes

www.ecb.europa.eu

ECB “Virtual Currency Schemes” (PDF) Review Guide: Everything You Need to Know + FAQ

What did Europe’s central bank really say about Bitcoin back when it was “just an experiment”—and why do people still quote that PDF today?

If you’ve tried to read the European Central Bank’s 2012 report “Virtual Currency Schemes,” you know the struggle. It’s formal, dense, and written before stablecoins, DeFi, MiCA, and the digital euro reshaped the conversation. Yet it’s one of the earliest official documents that tried to pin down what crypto is (and isn’t) for policymakers.

I’m here to make it simple, current, and useful. I’ll break the report into clear, modern takeaways: what the ECB nailed, what didn’t age well, how it connects to today’s rules, and the quick answers people keep searching for. Think of this as a fast pass through a long PDF—with the right context for 2025.

Why this often trips people up

- It’s from 2012: Bitcoin was barely on mainstream radar, so the report speaks to a world that didn’t know stablecoins, DeFi, or institutions holding BTC.

- Terminology is tricky: “Virtual currency,” “e-money,” and “legal tender” sound similar but mean very different things in EU law.

- It’s easy to misread the scope: The ECB looked at payments and financial stability, not investment returns or tech innovation.

- Context has shifted: MiCA is now live, AML rules got tougher (hello, travel rule), and the digital euro is in development—none of which existed when the report was written.

Quick example of the confusion I see all the time: someone says, “If my PayPal balance buys stuff, why isn’t Bitcoin the same?” Not quite. Your PayPal balance is typically e-money (regulated, redeemable at par, a claim on the issuer). Bitcoin is a virtual currency (not legal tender, no claim on an issuer). The ECB drew that line early, and EU regulation still follows it.

What you’ll get from this guide

- Plain-English mapping of what the ECB actually said (and what it didn’t).

- What holds up in 2025 and what needs updating in light of MiCA, AML/CFT, and the digital euro.

- Risk lens that still works: on/off-ramps, governance, user protections, and system impact.

- Fast navigation so you can skim the right sections of the PDF and move on with confidence.

- FAQ with straight answers, no jargon or hedging.

“Virtual currencies are not legal tender.” That early ECB line still defines the starting point for EU policy. Everything else—MiCA, licensing, AML—stacks on top of it.

Who this is for—and how to use it

- Investors and power users: spot where protections differ from banks, understand why exchanges and stablecoins face stricter rules now, and set your expectations on volatility and recourse.

- Builders and compliance teams: map your product to the report’s scheme types and governance models to anticipate supervision, AML pressure points, and MiCA obligations.

- Policy folks and researchers: use the ECB’s framework as a baseline, then layer in today’s data and rules to see how thinking evolved from “monitor” to “regulate.”

- Students and analysts: get a clean glossary, a reading plan, and the context to compare 2012 assumptions with 2025 reality.

I’ll keep this straight and practical—no academic fog, no crypto hype. Just the key ideas, real-world examples, and where they land in today’s landscape.

Ready to see what the ECB meant by “virtual currency,” where Bitcoin fit in their map, and why that still shapes EU rules today? Let’s start with what this paper actually is and why it matters next.

What is the ECB “Virtual Currency Schemes” paper and why it matters

The European Central Bank’s 2012 paper on “virtual currency schemes” was the first serious, structured look from a major central bank at Bitcoin and its peers. It set the baseline language Europe used for years: what these systems are, how people get in and out of them, and where the real risks sit. If you’ve ever argued about whether crypto is “money,” you’re quoting this report without realizing it.

“Virtual currency schemes are not money in the legal sense. They do not have the status of legal tender.”

— European Central Bank, 2012

I like this paper because it’s honest. Back then, Bitcoin was small, experimental, and messy. The ECB didn’t panic; it mapped the terrain and flagged what to watch. That mindset still holds up.

The short version

- Purpose-built map: The ECB explained how these schemes run, how users swap in and out of them, and who holds the keys (literally and figuratively).

- Clear legal line: Virtual currency isn’t legal tender and isn’t e-money. That line still shapes EU rules today.

- Risk scan: User scams, exchange failures, pseudonymity, and operational risks were the headline concerns.

- System impact in 2012: “Small but worth monitoring.” The ECB didn’t see a threat to monetary policy yet, but it kept the door open if usage grew.

Why the ECB wrote it

By 2012, Bitcoin had moved from mailing lists to mainstream tech press. People were buying and selling it on early exchanges and using it online. Some merchants started experimenting with it, and law enforcement had their eyes on it because of pseudonymous payments. Regulators needed a shared vocabulary and a common risk lens—fast.

- Define the thing: Without agreed definitions, every conversation turns into a semantic fight. The ECB cut through that.

- Spot the choke points: On- and off-ramps (exchanges, payment processors) were already the practical control layers. The paper called that out early.

- Protect the user: No chargebacks, no deposit insurance, and early exchange hacks meant real consumer harm if things went wrong.

It wasn’t a call to ban. It was a call to understand. And that tone ended up steering a lot of European policy thinking that followed.

Key terms: virtual currency vs e-money vs legal tender

This is the part people still get wrong in 2025, and the ECB’s definitions are sharp.

- Virtual currency: A digital value accepted by a community, not issued by a central bank or public authority, and typically usable within its own network. No legal tender status.

- Legal tender (in the euro area): Euro cash. You can offer it to settle debts, and it must be accepted within the legal framework.

- E-money (EU law): Digital value representing a claim on the issuer, issued on receipt of funds, and redeemable at par. It’s regulated under EU directives and, today, sits clearly under licensing and safeguarding rules.

In plain English: if you hold e-money, the issuer owes you euros back at 1:1 and must follow strict rules. If you hold virtual currency like Bitcoin, there’s no issuer and no claim. That difference still matters—right down to how today’s rules categorize stablecoins and who has to be licensed.

Questions this section helps answer

- What does “virtual currency” mean here? A privately issued, network-native unit that isn’t legal tender and doesn’t give you a right against an issuer.

- Is Bitcoin legal tender in the EU? No. It can be used if both sides agree, but it isn’t enforceable as legal tender.

- How is e-money different from crypto? E-money is a regulated claim on an issuer, redeemable at par. Crypto typically isn’t a claim and isn’t legal tender.

- Why did the ECB care back then? To build a shared map of the tech, find consumer and system risks, and watch the spots where crypto touches the traditional financial system.

“Not legal tender” might sound dry, but it’s the emotional heart of the early crypto story: freedom from gatekeepers also meant fewer safety nets. If you’ve ever lost funds on a dead exchange, you felt that sentence in your gut.

Here’s the fun part: once you understand the ECB’s definitions, you can sort any crypto system by how money moves and who’s in charge. Want a fast way to compare Bitcoin, game tokens, and today’s stablecoins using one simple lens? Let’s look at how the ECB split these schemes up—and why that still works shockingly well today.

How the ECB classifies “virtual currency schemes”

Here’s the mental model that still works in 2025: follow the money flows and look at who holds the keys. That’s exactly how the ECB sorted “virtual currency schemes,” and it’s still a sharp way to size up any token or platform in seconds.

“Follow the flow of money and you’ll find the risk.”

Closed, unidirectional, and bidirectional schemes

The ECB groups schemes by how value moves between fiat and the virtual world. It’s simple, and it explains 90% of where user risk and AML pressure points sit.

- Closed — value stays inside the platform. You can’t buy in with euros and you can’t cash out to euros.

Examples:- World of Warcraft Gold (in-game currency; any “cash-out” is against terms and relies on gray markets)

Why it matters: low external AML exposure, but high user exposure if the operator pulls the plug or changes rules. Your assets are stuck by design.

- Unidirectional — cash in, no official cash out. You can buy the currency, spend it in a walled garden, but you don’t redeem it for fiat.

Examples:- Facebook Credits (historical; users bought credits to spend on apps, no user redemption)

- Airline miles and many loyalty points (you purchase indirectly via activity, then spend, with no cash redemption)

Why it matters: AML risk is still mostly at the “cash-in” point; consumer risk shows up in value dilution (rule changes, expirations, devaluations).

- Bidirectional — cash in and cash out. The currency is exchangeable both ways through markets or official channels.

Examples:- Linden Dollars in Second Life (operator-managed markets let you buy and sell)

- Bitcoin via crypto exchanges (fully market-based entry and exit)

Why it matters: this is where consumer risk and AML/CFT supervision concentrate — on/off-ramps, exchanges, and payment integrations.

Even in 2012 the ECB placed Bitcoin squarely in the bidirectional bucket. That single decision explains why exchanges became the compliance choke point and why user losses historically centered on hacks and failures at those ramps, not on the base protocol.

Centralized vs decentralized governance

The second axis is governance. Who can change the rules, pause the system, or decide redemption terms?

- Centralized — a company runs it, defines the ledger, and can update terms. Think Linden Lab for Linden Dollars or any game studio for its in-game currency.

- Regulators see a clear counterparty. That means supervision and accountability flow to an operator.

- User protection depends on the operator’s solvency, security, and policies.

- Decentralized — no single operator; rules live in open-source code and distributed consensus. Bitcoin is the classic case.

- There’s no issuer to regulate directly, so oversight leans on service providers (exchanges, custodians, wallet providers).

- Tech risk shifts from corporate policy to protocol design and network security.

Note the mix-and-match: you can have a centralized + bidirectional scheme (Linden Dollars) or a decentralized + bidirectional scheme (Bitcoin). That blend is what determines where risk and responsibility sit.

Examples the ECB actually used

To ground the model, the paper leaned on recognizable systems:

- Closed: game currencies like World of Warcraft Gold (no official path to cash).

- Unidirectional: Facebook Credits (users bought credits to spend, no user redemption).

- Bidirectional, centralized: Linden Dollars (operator and official exchange).

- Bidirectional, decentralized: Bitcoin (peer-to-peer with exchanges as on/off-ramps).

If you’re wondering why law enforcement and compliance guidance later zeroed in on exchanges and custodians, this is why. The FATF’s VASP guidance repeatedly targets those bidirectional gatekeepers — the exact places where closed or unidirectional schemes don’t expose much surface area.

Why this still matters

Even with stablecoins and DeFi in the picture, this two-axis map is gold for fast risk triage:

- Consumer risk: Closed/unidirectional currencies concentrate risk in rule changes and redemption limits; bidirectional currencies add market risk and exchange failures.

- AML/CFT hotspots: Bidirectional flows create laundering routes; the choke points are issuers (if centralized) and service providers (if decentralized). That’s why travel rule obligations and KYC stack up there.

- Systemic spillovers: Bidirectional + broad integrations can transmit shocks into payment rails or liquidity venues. Decentralized systems push risk into protocol mechanics; centralized systems push it into issuer governance and reserves.

Try it on modern assets:

- USDC/USDT: bidirectional, centralized. Real-time blacklisting and issuer controls shape both user protection and AML reach.

- DAI: bidirectional with decentralized governance, but collateral includes centralized assets — a hybrid that mixes both oversight models.

- Game tokens with cash-out markets: often functionally bidirectional even if the T&Cs say otherwise — which is exactly where consumer disputes and fraud hotspots emerge.

The trick is to ask two questions: Can users cash out? and Who can change the rules? If you can answer those, you already know where to look for the weak links and which regulators will care.

So now that the map is clear, what did the ECB think could go wrong inside each box — for users, markets, and money itself? Let’s unpack the risks next, including a few the paper didn’t see coming.

The risks the ECB flagged (and what they missed)

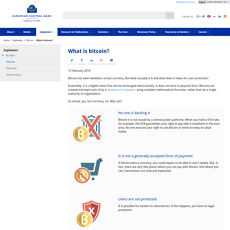

Consumer risks and investor protection

I remember reading this and nodding along. The ECB’s early warning was simple: crypto users don’t get the safety net they’re used to with banks and card networks. No chargebacks. No guaranteed recourse. If something breaks, you’re often on your own.

“Not your keys, not your coins.”

That line isn’t in the report, but it captures the heart of it. A few real-world reminders the ECB’s worries weren’t theoretical:

- Exchange failures and hacks: Mt. Gox collapsed in 2014, freezing user funds and rattling trust (BBC). Bitfinex was hacked in 2016. Fast forward, FTX imploded in 2022 with billions in customer assets missing. None of these came with consumer-style refunds.

- Volatility: 70%+ drawdowns have hit Bitcoin and other assets multiple times across cycles. If you needed to pay rent the next day, that price swing wasn’t just a chart — it was panic.

- Irreversibility and fake support: No chargebacks also means scammers love using crypto. If funds leave your wallet to a fraud address, the “refund department” is basically non-existent.

- Key loss: Lose your seed phrase, lose access. Independent analyses suggest millions of BTC are likely inaccessible. Chainalysis has tracked this problem for years.

Back in 2012, the ECB argued that users lacked the everyday protections they expected. A decade of headlines proved that point again and again.

AML/CFT and law enforcement visibility

The report zeroed in on the “pressure points”: exchanges and other on/off-ramps with weak KYC would be the choke points for laundering risk. It also flagged pseudonymity and easy cross-border transfers.

- Pseudonymous rails: On-chain activity is visible, but identities aren’t unless you attach them at an exchange or leave a breadcrumb trail.

- On/off-ramps: Where fiat meets crypto is where most AML obligations sit, and where the ECB expected regulators to focus.

- Data-backed reality: Illicit crypto volumes are a small share of total activity but still add up to tens of billions annually, according to the Chainalysis Crypto Crime Reports. That combination — low percentage, high absolute numbers — keeps AML/CFT concerns on the front burner.

The lesson the ECB wanted readers to get in 2012 still holds: if you want to reduce crime risk without crushing innovation, get serious at the gateways.

Operational and payment system risks

The paper talked about outages, wallet loss, and tech failures as user-level threats. None of that was theory.

- Wallet mistakes: Seed phrases lost, wrong addresses pasted, no safety net. A New York Times story even chronicled a multi-million dollar stash trapped behind a forgotten password — not rare, just vivid.

- Exchange outages during volatility: On busy days, big platforms have gone down or restricted trading. That can trap users in losing positions or block exits entirely.

- Network congestion: When transaction queues spike, fees surge. If your use case depends on fast, cheap settlement, high-fee periods can break the experience.

The ECB’s bottom line back then: these were real user risks, but the broader system wasn’t threatened — yet.

Monetary policy and financial stability

In 2012, crypto was tiny. The ECB’s view was that it posed no threat to monetary policy, with a caveat: if merchant acceptance expanded and networks scaled, the calculus might change. They were right to leave the door open. Changes in market size, leverage, and linkages to traditional finance turned out to matter a lot in later years.

What the ECB didn’t predict

To their credit, the ECB wasn’t trying to predict the future. Still, several huge shifts rewrote the risk map:

- Stablecoins as settlement rails: Fiat-referenced tokens became crypto’s “dollar on-chain.” That brought payment-like stability — and new fragility. Terra/UST’s 2022 collapse wiped out tens of billions and triggered a cascade (BIS). Even reserve-backed coins have wobbled: USDC temporarily broke its peg during the SVB shock (Reuters).

- DeFi composability and cascade risk: Stacking protocols is powerful — and brittle. Oracles fail, collateral drops, liquidations spiral, and losses propagate across apps. Central bankers now track these “hidden interconnections” in detail (BIS: The decentralisation illusion).

- Global crypto market cycles with real contagion: The 2022 unwind hit lenders, exchanges, and funds in rapid sequence. The FSB now warns that as traditional finance linkages grow, these runs can spill over.

All of this didn’t exist on the ECB’s radar in 2012, which is fair. But it’s also why it’s risky to judge today’s market with a 2012 lens alone.

If the report nailed the early warning signs, which parts still hold up in 2025 — and which ones need a hard update? I’ll show you exactly what aged well and what changed next.

2012 vs today: what aged well and what changed

What aged well

I still reach for the ECB’s 2012 lens when I’m trying to quickly understand a new crypto product. Some parts are timeless, and they keep proving useful in 2025:

- Definitions that don’t wobble: The line between legal tender, e‑money, and “virtual currency” was crystal clear back then and it still guides EU rules today. It’s why a euro is different from Bitcoin, and why a regulated e‑money token isn’t just “another coin.”

- On/off‑ramp focus: The report zoomed in on exchanges and gateways as the real choke points. Fast forward: AML rules and the Travel Rule now live right there, and that’s where most compliance work happens.

- Consumer risk themes: Price swings, irreversible transactions, wallet loss, and exchange failures were flagged early. Mt. Gox made it obvious in 2014; FTX hammered it home in 2022. Same patterns, different names.

- Centralized vs decentralized governance: Whether there’s an operator (custodial stablecoin, centralized exchange) or not (Bitcoin, most base-layer networks) still determines who regulators can hold responsible and how safeguards are designed.

“Given their limited connection with the real economy, virtual currency schemes do not pose a risk to price stability at this stage… but they should be monitored.” — ECB, 2012

That sentence aged surprisingly well as a mindset: don’t panic, don’t ignore — monitor and measure.

What’s outdated or incomplete now

Plenty changed. Some of the most important shifts weren’t on anyone’s radar in 2012:

- Stablecoins are now the payment rail: Trillions of dollars in stablecoin transfers move each year on public chains (see Coin Metrics). This flips the original “too small to matter” view and pulls stablecoins directly into payments, treasury, and market liquidity conversations.

- DeFi rewired market plumbing: Automated market makers, lending protocols, and on‑chain collateral changed how liquidity forms. DeFi total value locked has swung from tens of billions to over $100B across cycles (DefiLlama). None of this was in the 2012 playbook.

- Institutional scale is real: Spot bitcoin ETFs in major markets and regulated custodians with insurance, SOC audits, and segregation are normal now. The paper didn’t anticipate that kind of mainstream market integration.

- Risk vectors evolved: The report focused on exchange hacks and user mistakes. Today we add oracle manipulation, bridge exploits, MEV, governance attacks, and stablecoin depegs (remember TerraUSD in 2022).

- Data changed the compliance debate: Blockchain analytics made “anonymous money” a weaker claim. Illicit activity is a small slice of volume by share, even if absolute numbers are big (Chainalysis 2024).

Today’s landscape: MiCA, AML, and CBDC

EU rules now put structure where the 2012 paper saw ambiguity:

- MiCA (Reg. (EU) 2023/1114): Issuers and service providers have clear obligations. Stablecoins are split into e‑money tokens (EMTs) and asset‑referenced tokens (ARTs) with reserve, redemption, and disclosure rules. Stablecoin provisions started applying in mid‑2024; broader CASP licensing kicks in from late 2024 (EUR‑Lex).

- AML + Travel Rule (Reg. (EU) 2023/1113): Crypto transfers need originator/beneficiary information, and CASPs face enhanced checks for interactions with self‑hosted wallets in riskier scenarios. This pushes real compliance to the exact spots the ECB warned about in 2012 — the on/off‑ramps (EUR‑Lex).

- Supervision and thresholds: “Significant” stablecoins face tighter oversight, extra reporting, and potential usage thresholds that trigger more scrutiny (see the EBA’s MiCA package and consultation papers on ART/EMT supervision; EBA).

- Digital euro: The ECB moved into a multi‑year preparation phase to build a retail CBDC with privacy features and offline options, intermediated by supervised payment providers (ECB). Back in 2012, a euro CBDC wasn’t even part of the conversation.

Put differently: the EU now has a rulebook and is prototyping its own digital cash, while the private crypto market built global, 24/7 settlement rails in parallel.

Should you still read it?

Yes — not for up‑to‑the‑minute rules, but as a clean mental framework for mapping money flows, governance, and risk points. I still use it to sanity‑check new products: Where do funds enter and exit? Who’s accountable? What breaks if this operator goes down? How do consumers get made whole?

“If the thesis is still useful after the facts change, you’ve got a keeper.” This paper is a keeper — as long as you pair it with MiCA, today’s AML requirements, and the lessons from 2017–2024 market cycles.

Want the fastest way to apply this without getting stuck in a 50‑page PDF? In the next section I’ll show you a quick path through the report and turn it into a checklist you can actually use. Which one do you want first — the 10‑minute skim plan or the role‑by‑role takeaways?

Practical takeaways and how to read the PDF fast

Here’s how I actually use the ECB’s “Virtual Currency Schemes” in 2025: as a tactical checklist. The paper is old, but the mental models are crisp. If you’re using crypto, building in it, or researching policy, this is how to turn that PDF into real decisions.

For crypto users and investors

The ECB’s core warning still lands: you don’t get bank-grade protections in crypto. Treat your setup like a self-managed security stack.

- Use regulated on/off-ramps. In the EU, look for registered CASPs and payment partners with real KYC and incident reporting. That’s where AML/CFT controls live—and where your recourse starts if something goes wrong.

- Verify custody, not vibes. If an exchange or broker holds your coins, look for independent audits, asset segregation, and a proof-of-reserves + proof-of-liabilities approach (both sides matter). A Merkle tree without an auditor is marketing.

- Expect volatility and liquidity breaks. Even “stable” assets can wobble—remember the USDC weekend depeg in 2023. Keep a cash buffer and split positions across venues so one outage doesn’t trap you.

- Assume no chargebacks. Crypto rails don’t do friendly fraud. Double-check addresses, use small test sends, and add withdrawal address whitelists and time locks.

- Keep core funds in self-custody. Hardware wallet + strong passphrase + offline backups. Exchanges are for liquidity, not long-term storage.

- Be scam-stubborn. Chainalysis reports repeatedly show billions lost to hacks and scams each year. If someone rushes you to “move funds now,” stop. Good opportunities survive scrutiny; bad ones need speed.

Quick mental model: Treat centralized platforms like banks for UX and liquidity—but not for guarantees. Treat self-custody like a safe—you own the security story.

For founders and compliance teams

Use the ECB’s classification as a design radar. Where money can enter/exit and who controls the system dictates your risk and regulatory obligations.

- Map your scheme type. Are you closed (no fiat in/out), unidirectional (fiat in only), or bidirectional (fiat both ways)? Bidirectional + consumer-facing = your heaviest controls and supervision points.

- Be honest about governance. If there’s a company running matching engines, oracles, or upgrades, you’re centralized in the eyes of a supervisor—no matter how many nodes you cite. Build controls for that reality.

- On/off-ramp-grade compliance. Strong KYC, sanctions screening, blockchain analytics, and the EU Transfer of Funds Rule (Travel Rule) data flows. Automate transfer screening and case management early, not after the first regulator email.

- Segregate customer assets. Separate wallets, robust key ceremonies, hardware-backed HSMs, and withdrawal policies that require multi-person approval. Publish clear recovery and incident procedures.

- Proof you can redeem. If you issue tokens, independent attestations of reserves and liquid backing (frequency, custody location, maturity profile). MiCA raises the bar—act like it’s already in force.

- Kill-switches with sunlight. If you implement circuit-breakers, document triggers and publish them. Users forgive risk controls; they don’t forgive opaque freezes.

- Tabletop your worst day. Run practice drills: exchange outage, oracle failure, liquidity crunch, key compromise. Time your mean-time-to-pause, mean-time-to-communicate, and mean-time-to-restore. Then shrink them.

- Measure what supervisors care about. Track concentration risk (top counterparties, top wallets), liquidity ladders, fraud loss rates, SAR volumes, and uptime. What gets measured gets managed—and licensed.

For researchers and students

I use the 2012 paper as a baseline to show how the narrative moved from “niche experiment” to “regulated market.” It’s ideal for comparisons and trend analysis.

- Replicate the taxonomy on today’s systems. Classify stablecoins, bridges, and DeFi protocols using the ECB’s scheme types + governance lens. Where do hybrids (e.g., centralized issuers with decentralized rails) land?

- Event studies worth running. Price, volume, and on-chain flow shifts around depegs, exchange outages, and policy announcements. Look for spillovers between tokens and between centralized vs decentralized venues.

- Data sources to triangulate. On-chain explorers, public exchange volumes, market microstructure feeds (e.g., order book depth), and policy timelines. Add enforcement action dates to your regression calendar.

- Policy evolution timeline. Start with the ECB’s definitions, then trace to MiCA categories, AML updates, and CBDC papers. Your conclusion writes itself: language hardened into law.

Quick path through the PDF

Short on time? Here’s my speed run that still preserves the signal:

- Executive Summary: Get the thesis and the early risk map in minutes.

- Definitions: Lock in the distinction between virtual currency, e-money, and legal tender—this frames every later rule.

- Classification: Note the closed/unidirectional/bidirectional split and centralized vs decentralized governance. Keep that model in your notes.

- Risk Assessment: Read line by line. Tag each risk (consumer, AML/CFT, operational, systemic) and write a 1-sentence “today” update next to it.

- Skim legacy examples: Useful context, but don’t get stuck—translate the logic to today’s products as you go.

Pro tip: open the PDF and use CTRL/CMD+F for these keywords—“bidirectional,” “decentralised,” “risks,” “e-money.” You’ll jump straight to the meat.

Where to read it

ECB PDF: https://www.ecb.europa.eu/pub/pdf/other/virtualcurrencyschemesen.pdf

Skim it with these notes in hand and you’ll get what you need in under an hour. Want the instant answers to the questions people ask about this paper—like legal tender status and whether the ECB ever pushed for a ban? That’s up next in the FAQ. Ready for the fastest yes/no section you’ll read all week?

FAQ: ECB Virtual Currency Schemes — quick answers

Is virtual currency legal tender in the EU?

No. The ECB made it plain back in 2012 and it’s still the case today: legal tender in the euro area is euro banknotes and coins. Crypto is something you can choose to accept, not something anyone can force on you for payments or debts.

- Example: a café in Lisbon can accept Bitcoin via a payment processor, but tax, fines, and most official fees still have to be paid in euros.

- Outside the EU you’ll find different rules (e.g., El Salvador made BTC legal tender), but that doesn’t change the EU position.

ECB explainer on legal tender: ecb.europa.eu

What’s the difference between virtual currency and e-money?

Think “claim and redemption” vs “no claim.”

- E-money: Regulated under EU law. It represents a claim on the issuer, is issued on receipt of funds, and is redeemable at par at any time. Examples: your Revolut/PayPal EUR balance or a regulated prepaid card balance. Law: EMD2, Directive 2009/110/EC.

- Virtual currency: No legal claim on an issuer and not legal tender. Examples: BTC, ETH. Price floats with the market, and there’s no guaranteed redemption.

- Stablecoins today: Under MiCA, a euro-denominated “e-money token” (EMT) must be issued by an authorized e-money institution and provide par redemption rights—functionally closer to e-money. Not every stablecoin meets this bar; some are “asset-referenced tokens” (ARTs) with different rules, and many non‑EU stablecoins are not e-money in the EU.

Did the ECB call for banning crypto in this paper?

No. The message was “monitor and assess,” not “ban.” The EU path since then has been to regulate instead of prohibit.

- MiCA sets rules for issuers and crypto-asset service providers: EUR‑Lex

- Travel Rule/TFR extends AML requirements to crypto transfers: Regulation (EU) 2023/1113

- DAC8 adds tax reporting by crypto platforms: Directive (EU) 2023/2226

That approach answers the risks the ECB flagged (consumer protection, AML, operational chokepoints) without shutting down innovation.

Final take

Use the paper as a map, not the destination. The definitions still help you think clearly; the rules you need to act on live in MiCA, AML, and today’s supervisory guidance.

If you’re paying or building with crypto in the EU, anchor yourself in three checks: Is it legal tender? Is there a claim and par redemption? Which rulebook applies (MiCA/EMD2/AML)? Answer those fast, and you’ll make smarter, safer choices.

Source PDF: ECB — Virtual Currency Schemes (2012)