CASHCAT’s Robinhood Chain Surge: How an $838 Trade Topped $1M—and Why Liquidity Matters

0x020bfC650A365f8BB26819deAAbF3E21291018b4, traded near $0.0964 with a market capitalization of approximately $95 million at the time of our snapshot. That was roughly 58% below its July 11 peak near $0.2288.One early wallet reportedly converted an $838 purchase into approximately $917,600 of gross sale proceeds while retaining a six-figure position. However, CASHCAT was not created or endorsed by Robinhood, and its principal liquidity pool of roughly $7.5 million remained far smaller than the token’s displayed valuation.

Key takeaways

- CASHCAT is an independently deployed memecoin trading on Robinhood Chain, not an official Robinhood token or Stock Token.

- An early buyer reportedly spent $838, sold most of the position for approximately $917,600 and retained about 1.54 million CASHCAT.

- The widely repeated $1 million result combines realized proceeds with unsold tokens whose value remained exposed to the market.

- CASHCAT’s principal Uniswap V3 pool held approximately $7.5 million of liquidity against a market capitalization near $95 million.

- Market-depth estimates showed only about $155,000 of liquidity within 2% of the quoted price on either side of the principal market.

- Robinhood Chain recorded substantial early DEX activity, but volume, transactions and address counts do not by themselves prove durable economic adoption.

What is CASHCAT on Robinhood Chain?

CASHCAT is a cat-themed memecoin built around a real piece of Robinhood history. Before Robinhood settled on its current name and branding, its founders reportedly considered “Cash Cat” and a mascot depicting a cat holding cash.

That origin gave the token a more recognizable narrative than a randomly generated ticker. CASHCAT appeared on Robinhood’s newly launched blockchain, referenced an abandoned company concept and provided traders with an immediately understandable mascot.

The first distinction I would make is between Robinhood Chain and Robinhood’s own products.

Robinhood Chain is a permissionless, Ethereum-compatible Layer 2 built using Arbitrum technology. It uses ETH for gas, supports EVM smart contracts and permits independent developers to deploy applications and tokens without Robinhood approving each deployment.

Anyone being allowed to create a token is a feature of a permissionless network. It is not evidence that Robinhood reviewed, issued or endorsed that token. Readers unfamiliar with the architecture can consult our guide to how Ethereum Layer 2 networks work.

CASHCAT is not an official Robinhood token

Robinhood launched Robinhood Chain. Robinhood did not launch CASHCAT.

CASHCAT does not represent Robinhood Markets shares, voting rights, revenue, dividends or economic ownership in Robinhood. It is also separate from Robinhood’s Stock Tokens, which are structured products intended to provide economic exposure to referenced securities under specific terms and restrictions.

The token is not protected by FDIC insurance or SIPC protection. A token existing on Robinhood Chain is also not automatically listed in Robinhood’s brokerage or crypto application.

| Claim | Verdict | Explanation |

|---|---|---|

| Robinhood created CASHCAT | False based on available evidence | CASHCAT was independently deployed on a permissionless network. |

| CASHCAT trades on Robinhood Chain | True | The token and principal trading pool are visible through Robinhood Chain market and explorer data. |

| CASHCAT represents Robinhood equity | False | It provides no shareholder, voting or dividend rights. |

| CASHCAT is a Robinhood Stock Token | False | It is a memecoin and belongs to a separate asset category. |

| Vlad Tenev acknowledged meme activity | True | He publicly acknowledged that Robinhood Chain was also being used for memes. |

| Vlad Tenev formally endorsed CASHCAT | Unverified | A category-level comment or social-media follow is not a formal token endorsement. |

| Robinhood audited CASHCAT | No evidence found | Permissionless deployment does not imply Robinhood reviewed the contract. |

Robinhood’s official mainnet announcement positioned the chain around tokenized real-world assets, Stock Tokens, lending, self-custody and other financial applications. CASHCAT’s speculative rise unfolded on top of that infrastructure, but it is not one of Robinhood’s financial products.

How an $838 purchase became a seven-figure position

The wallet behind the headline reportedly spent approximately $838 to acquire 15.04 million CASHCAT. It later sold roughly 13.5 million tokens for approximately $917,600, leaving about 1.54 million tokens.

At the July 9 snapshot reported by CoinDesk, the remaining tokens were valued at approximately $133,700. Adding that paper value to the gross proceeds produced a total marked result of approximately $1.051 million.

| Component | Amount | Status | Important limitation |

|---|---|---|---|

| Initial purchase | Approximately $838 | Realized expense | The precise ETH-to-USD conversion time affects the dollar cost. |

| CASHCAT acquired | 15.04 million | Historical | Related purchases or wallets could affect a complete cost basis. |

| CASHCAT sold | Approximately 13.5 million | Realized disposal | The sales may have occurred across multiple swaps. |

| Gross sale proceeds | Approximately $917,600 | Realized | Gross proceeds are not the same as net profit. |

| Estimated acquisition cost allocated to sold tokens | Approximately $752 | Realized cost | Uses a proportional cost-basis calculation. |

| Estimated realized gain before fees | Approximately $916,848 | Realized estimate | Excludes swap, gas, bridge, routing and tax costs. |

| Remaining tokens | Approximately 1.54 million | Unrealized at the July 9 snapshot | The wallet balance may subsequently have changed. |

| Remaining paper value | Approximately $133,700 | Unrealized | The full position might not be sellable at the quoted price. |

| Total marked value | Approximately $1.051 million | Mixed | Combines proceeds already received with continuing market exposure. |

The million-dollar headline is directionally accurate, but it combines three different concepts:

- Gross proceeds already received from token sales.

- Estimated profit after accounting for acquisition and transaction costs.

- The paper value of tokens that had not yet been sold.

The wallet achieved an exceptional result. That does not make its experience representative of the median CASHCAT trader.

Realized profit and paper value are not the same

A token balance multiplied by the latest quoted price creates a marked value. It does not guarantee that the full balance can be sold at that price.

A large swap moves through a decentralized exchange pool’s pricing curve. The seller receives progressively worse prices as the trade consumes available liquidity, particularly when liquidity is concentrated inside narrow Uniswap V3 ranges.

Our Uniswap review and liquidity explanation covers how automated liquidity pools differ from conventional order books. With CASHCAT, that difference is central to understanding the million-dollar claim.

At the July 16 snapshot, the main CASHCAT/WETH pool held approximately $7.54 million of liquidity. CoinGecko’s market data showed only about $155,000 of quoted depth within 2% of the principal market price on either side.

A seller does not need to drain the entire pool to produce significant price impact. Final proceeds depend on:

- the amount of active liquidity inside the current price range;

- the size of the sale;

- the trader’s slippage tolerance;

- competing sellers and arbitrage activity;

- routing through secondary pools;

- gas and bridge costs; and

- centralized-exchange order-book depth.

Did CASHCAT really rise more than 4,000%?

Yes, CASHCAT moved by more than 4,000% across several defensible historical windows, but every percentage claim needs a specific starting price, ending price and timestamp.

CoinGecko recorded an early July 1 price near $0.001604 and an all-time high near $0.2288 on July 11. Using those figures:

Percentage gain = ($0.2288 − $0.001604) ÷ $0.001604 × 100 = approximately 14,164%.

Other platforms recorded different opening prices and slightly different peaks. This disagreement illustrates the problem with using the first trades in a newly created pool as a universal performance benchmark.

Initial liquidity may have been extremely small. A modest purchase could have moved the price sharply, while the earliest displayed quote might not have supported meaningful trade size.

I would therefore treat “up 4,000%” as a historical return across a specified period, not as a permanent characteristic of CASHCAT. By July 16, the token was already more than 57% below its recorded peak.

What drove the CASHCAT rally?

CASHCAT benefited from several overlapping catalysts rather than one provable cause:

- Robinhood Chain’s July 1 public-mainnet launch;

- the token’s connection to Robinhood’s abandoned Cash Cat concept;

- a simple and recognizable mascot;

- rapid early price appreciation;

- DEXScreener visibility and social-media attention;

- additional token-launch and exchange access;

- reported perpetual-futures trading; and

- the broader appetite for first-mover memecoins on new networks.

The timing suggests these developments helped expand attention and market access, but the available evidence cannot isolate a single cause. An exchange or derivatives listing can make a token easier to trade without proving that demand is organic or sustainable.

Vlad Tenev acknowledged memes—but did he endorse CASHCAT?

Robinhood CEO Vlad Tenev said shortly after the chain’s launch that assets without utility did not serve a lasting purpose. Days later, as memecoin activity increased, he wrote that Robinhood was building the chain for real-world assets but that it “works great for memes too.”

That comment acknowledged how the permissionless network was being used. It was not a formal statement that Robinhood created, audited, listed or guaranteed CASHCAT.

Tenev also reportedly followed the token’s social-media account. Following an account does not amount to company approval. I would not describe CASHCAT as Robinhood-endorsed without a formal statement from Robinhood identifying it as such.

The liquidity behind CASHCAT’s market cap

| Metric | July 16 snapshot | What it shows | What it does not prove |

|---|---|---|---|

| Price | Approximately $0.096 | The latest marginal trade price | The price available for an entire large position |

| Market capitalization | Approximately $95 million | Price multiplied by estimated circulating supply | The amount of cash invested in CASHCAT |

| Fully diluted valuation | Approximately $95 million–$97 million | Price multiplied by total token supply | Guaranteed exit value |

| Main-pool liquidity | Approximately $7.54 million | Assets supporting swaps in the principal pool | Guaranteed redemption at the displayed price |

| Main-pool 24-hour volume | Approximately $32 million | Trading turnover during the rolling period | Net inflows or new capital |

| Main-pool traders | Approximately 4,093 addresses | Addresses classified as traders | 4,093 unique people |

| Depth within 2% | Approximately $155,000 per side | Estimated executable size close to the quoted price | Future depth or liquidity during a sell-off |

| Decline from all-time high | Approximately 57%–58% | The size of the retracement from the July 11 peak | Where the price will move next |

The main pool’s liquidity-to-market-cap ratio was approximately 7.9%. Its 24-hour volume-to-liquidity ratio was approximately 4.25 times, showing that the pool’s assets turned over several times during the rolling period.

High turnover proves that substantial trading occurred. It does not prove that an equivalent amount of fresh capital entered the token.

Why early wallets can exit while late buyers struggle

Early buyers enter when a token’s absolute value and liquidity are small. A relatively modest purchase can acquire a large token balance.

As later buyers arrive, the token’s price and displayed market capitalization rise. Early wallets can then sell portions of their holdings into the new demand. The later buyers become counterparties to the early exits.

| Example | Entry | Position | Possible result | Main constraint |

|---|---|---|---|---|

| Reported early wallet | Approximately $838 | 15.04 million CASHCAT | More than $1.05 million in combined proceeds and paper value at the July 9 snapshot | The position was acquired before broad demand arrived. |

| Hypothetical later buyer | $10,000 at $0.10 | Approximately 100,000 CASHCAT before fees | Approximately $5,000 after a 50% price decline | The entry occurred after valuation and attention had expanded. |

| Hypothetical large holder | 1.54 million tokens marked near $0.096 | Approximately $147,800 displayed value | Actual proceeds depend on execution | Selling the full position can move the pool price. |

This is a hypothetical illustration, not a forecast or trading recommendation.

The early-wallet stories show what was possible for a handful of addresses. They do not reveal the median trader’s return, the number of wallets that lost money, the percentage of buyers who entered above the current price or how much of each displayed position could be sold.

That is survivorship bias. Exceptional winners become headlines. Ordinary losses and failed token launches usually receive far less attention.

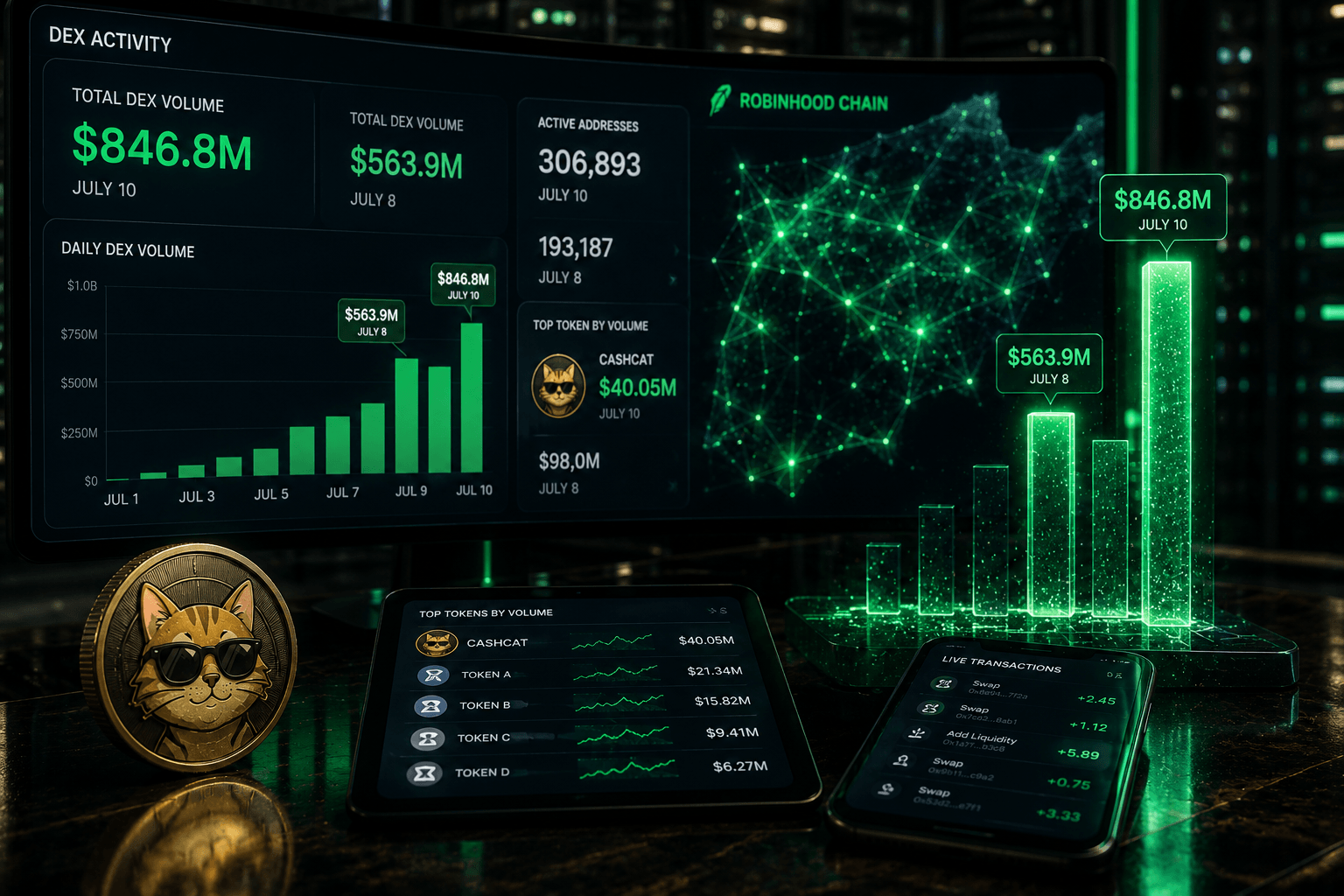

What Robinhood Chain’s record DEX volume actually shows

Reported Dune data showed Robinhood Chain’s daily decentralized-exchange volume reaching approximately $563.9 million on July 8 and $846.8 million on July 10.

| Date | Reported DEX volume | Reported active addresses | Reported new addresses | Reported CASHCAT volume | Approximate CASHCAT share |

|---|---|---|---|---|---|

| July 8, 2026 | $563.9 million | 193,187 | More than 140,000 | Approximately $98 million | Approximately 17.4% |

| July 10, 2026 | $846.8 million | 306,893 | 153,332 | Approximately $40.05 million | Approximately 4.7% |

These are meaningful activity figures for a recently launched chain, but they require qualification.

Addresses are not necessarily people. One trader can control numerous wallets. Bots, arbitrageurs, market makers and transaction routers can generate substantial activity. DEX turnover may also represent the same capital changing hands repeatedly.

Trading volume is not equivalent to bridge inflows, total value locked, stablecoin liquidity or retained economic activity.

For me, the chain-level story is more important than the cat. The durable indicators will be returning users, stablecoin liquidity, bridge flows, fee generation and real-world-asset activity after memecoin prices cool.

Contract, holder and liquidity risks

The CASHCAT name or logo is not enough to identify the token. Unrelated contracts can use the same name or ticker on Solana, BNB Chain and other networks.

The Robinhood Chain contract reviewed for this article is:

0x020bfC650A365f8BB26819deAAbF3E21291018b4

The principal reviewed CASHCAT/WETH Uniswap V3 pool is:

0xa70fc67c9f69da90b63a0e4c05d229954574e313

Readers can inspect the token through Robinhood Chain Blockscout and compare the pool through DEXScreener or GeckoTerminal.

CryptoLinks maintains a directory of token, rug-pull and liquidity-pool security scanners, but an automated score is not the same as a professional smart-contract audit.

At the time of publication:

- no definitive independent professional audit was confirmed;

- a complete review of minting, proxy, blacklist, pause and fee-changing privileges remained outstanding;

- ownership of the principal Uniswap V3 position NFTs was not independently established;

- no claim that the liquidity is permanently locked or burned could be verified;

- holder-count platforms disagreed substantially; and

- a reliable top-10 concentration calculation excluding pools, exchanges and contract addresses was unavailable.

Uniswap V3 liquidity is represented through concentrated-liquidity positions rather than traditional fungible LP tokens. Claims that “the LP was burned” should not be repeated unless the position ownership and withdrawal controls have been verified directly.

Is CASHCAT the start of a corporate-chain memecoin meta?

CASHCAT may be the first strong example of a permissionless memecoin becoming an unofficial cultural asset for a newly launched, institutionally oriented blockchain.

The constructive interpretation is that CASHCAT created recognizable native culture, attracted substantial liquidity and demonstrated that Robinhood Chain is genuinely open to independent developers.

The skeptical interpretation is that one successful token does not establish a durable market category.

A broader corporate-chain memecoin trend would require:

- several successful tokens rather than one;

- liquidity that remains after prices decline;

- returning users and stable holder retention;

- declining concentration among early wallets;

- community tools and independent developers;

- sufficient stablecoin and bridge liquidity;

- reliable exchange access; and

- communities that survive without executive attention.

Similar dynamics have appeared in other major memecoin ecosystems, particularly on networks where inexpensive, permissionless token creation attracts speculative activity.

The unusual element in this case is the contrast between Robinhood’s institutional real-world-asset strategy and the unofficial memecoin that first captured widespread retail attention.

The strongest case for CASHCAT

The bullish case is cultural rather than fundamental.

CASHCAT has a verifiable Robinhood origin story, a recognizable identity and first-mover status on Robinhood Chain. It attracted meaningful liquidity, trading volume and exchange attention. Nearly the entire supply also appeared to be circulating based on available aggregator data, which could reduce conventional vesting-unlock risk if the supply methodology is correct.

Continued growth in Robinhood Chain usage could preserve attention around its first major native meme. The token also demonstrates that Robinhood Chain’s permissionless deployment model works as advertised.

The strongest case against CASHCAT

CASHCAT provides no ownership claim on Robinhood, no verified revenue and no underlying asset value.

Its price rose much faster than its liquidity. Early-wallet profits came from later counterparties, while marked wallet values may not be fully realizable. Concentrated liquidity can move or be withdrawn, derivatives can amplify volatility and Robinhood Chain itself has a limited operating history.

The token also faces:

- anonymous or unidentified-deployer risk;

- copycat contracts and fake airdrops;

- possible holder concentration;

- bridge and sequencer risk;

- smart-contract vulnerabilities;

- leveraged-liquidation risk; and

- dependence on continued Robinhood-related attention.

Readers should compare every token link against the full contract address and review our cryptocurrency scam and suspicious-site list before connecting a wallet. Our crypto wallet guide also explains the differences between self-custody and platform custody.

Three outcomes to watch next

Scenario A: CASHCAT becomes Robinhood Chain’s lasting cultural token

Liquidity remains stable, holder concentration declines, trading continues after social attention cools and community development becomes independent of Robinhood executives.

Scenario B: CASHCAT remains a successful but temporary launch meme

The token retains some liquidity and cultural recognition but loses its position as the chain’s dominant narrative as real-world assets, stablecoins and newer tokens attract attention.

Scenario C: Liquidity and attention unwind together

Whale selling, falling volume, derivatives liquidations or liquidity withdrawals accelerate the decline. A competing token or a renewed focus on Robinhood’s Stock Tokens could weaken the CASHCAT narrative further.

These scenarios are analytical frameworks, not price predictions.

Conclusion: the gain is real, but the headline hides the exit problem

The $838 trade is a legitimate illustration of what extreme early positioning can produce in a newly launched, thin market. The wallet reportedly received almost $918,000 from sales and still held a substantial token balance at the July 9 snapshot.

However, “$838 became $1 million” compresses gross proceeds, unrealized value and execution risk into one sentence.

What stands out to me is the gap between CASHCAT’s displayed market capitalization, its total pool liquidity and the actual depth available close to the quoted price.

CASHCAT has already succeeded as Robinhood Chain’s first major cultural breakout. Whether that success develops into a lasting community remains unresolved. It should not be confused with an official Robinhood investment product or with evidence that late buyers can reproduce the entries and exits achieved by the earliest wallets.

The metric I would monitor next is retained liquidity—not social impressions.

Frequently asked questions

What is CASHCAT?

CASHCAT is an independently deployed memecoin trading primarily on Robinhood Chain and through supported external markets.

Is CASHCAT an official Robinhood token?

No. Robinhood launched Robinhood Chain, but available evidence shows that independent developers created CASHCAT.

What is the correct CASHCAT contract address?

The Robinhood Chain contract reviewed for this article is 0x020bfC650A365f8BB26819deAAbF3E21291018b4.

Did a trader really turn $838 into more than $1 million?

Yes, based on the reported July 9 snapshot. The calculation combined approximately $917,600 of gross sale proceeds with an unsold position then valued near $133,700.

Was the entire $1 million realized profit?

No. Part of the total represented gross proceeds and part represented paper value. Acquisition costs, trading fees, gas, bridge costs and taxes also reduce net profit.

Did CASHCAT really gain more than 4,000%?

Yes, across some historical periods. The exact percentage varies substantially according to the starting trade, timestamp and liquidity available at the beginning of the selected period.

Why did CASHCAT rise?

CASHCAT rose amid Robinhood Chain’s launch, its verifiable Cash Cat origin story, rapid early appreciation, social attention and expanded market access. No single catalyst can be proven to have caused the full rally.

Did Vlad Tenev endorse CASHCAT?

No formal endorsement was identified. Tenev acknowledged meme activity on Robinhood Chain, but that is not equivalent to Robinhood issuing or approving CASHCAT.

How much liquidity does CASHCAT have?

The principal CASHCAT/WETH pool held approximately $7.54 million at the July 16, 2026 snapshot. The value changes continuously.

Can a large CASHCAT holder sell at the displayed price?

Not necessarily. A large sale can move the pool price and produce significantly lower average execution because of price impact and slippage.

Is CASHCAT available in the Robinhood app?

An official in-app CASHCAT listing was not independently confirmed. Trading on Robinhood Chain does not automatically mean a token is listed in Robinhood’s brokerage or crypto application.

Is CASHCAT a Robinhood Stock Token?

No. CASHCAT is a memecoin and does not provide the rights or economic structure associated with Robinhood’s Stock Tokens.

Is the CASHCAT contract audited?

A definitive independent professional audit was not confirmed. Automated scanner results should not be described as complete smart-contract audits.

What network fees are needed to trade CASHCAT?

Robinhood Chain uses ETH as its native gas asset. Swaps can also involve pool fees, price impact, slippage, bridge costs and routing fees.

How can users avoid fake CASHCAT tokens?

Verify the network and full contract address before interacting. Do not rely solely on a ticker, token name, logo or link received through an unsolicited message.

Sources and methodology

Market figures were recorded between 08:38 and 08:56 UTC on July 16, 2026. The principal Uniswap V3 pool was treated as the primary spot-price source, with GeckoTerminal, CoinGecko and other aggregators used for comparison.

Market capitalization and fully diluted valuation were not treated as invested capital or realizable value. Trading volume was not treated as net capital inflow.

The featured-wallet reconstruction uses CoinDesk’s July 9 reporting, which attributed its figures to on-chain DEXScreener data. Gross proceeds, estimated profit and unsold paper value were calculated separately.

- Robinhood Chain public-mainnet announcement

- Official Robinhood Chain documentation

- Robinhood Chain Blockscout CASHCAT page

- DEXScreener CASHCAT/WETH pool

- GeckoTerminal CASHCAT/WETH pool

- CoinGecko CASHCAT market data

- CoinDesk early-wallet analysis

- Dune-derived Robinhood Chain activity reporting

Disclosure: This article is for informational purposes only and does not constitute investment, financial, legal or tax advice. Memecoins can be extremely volatile, and displayed token values may not be realizable during periods of limited liquidity.