Tom Lee Says ETH Can Hit $60K in 2026: What He Told Paris Blockchain Week, What Institutions Hear, and What I’m Watching

What if we’re going to look back at today and say, “Yep… that was the moment Ethereum stopped trading like a crypto project and started trading like financial infrastructure”?

That’s basically the tension behind Tom Lee’s $60K ETH call. If he’s even half right, the upside from here isn’t a cute swing trade — it’s a full reset in how the market values Ethereum.

But here’s the problem: most people don’t actually know how to value ETH in the first place. They just argue the number.

If we can’t agree on what ETH is, we’ll never agree on what ETH is worth.

So before we get excited (or dismissive), I want to make this practical: why valuing Ethereum is confusing, what frameworks actually matter, and how to translate a headline like “$60K ETH” into a checklist you can verify instead of pure hype.

The real problem: most people still don’t know how to value Ethereum

Ethereum is one of the only assets I can think of that behaves like multiple asset classes at once:

- A tech platform (apps get built on it, developers choose it, upgrades matter)

- A fee economy (users pay to move value, use apps, settle trades)

- A monetary asset (ETH is held, staked, used as collateral, used as “money” inside crypto)

- A settlement layer (stablecoins, tokenized assets, and institutions care about finality + reliability)

That mix is why people keep making bad comparisons like:

- “It’s just like Bitcoin” (it isn’t)

- “It’s just like a tech stock” (also not true)

- “It’s just another L1” (ignores the network effect + capital gravity)

And it’s why institutions often sound like they’re speaking a different language than retail. Retail usually asks: “When moon?” Institutions ask: “What’s the repeatable value capture mechanism, and can we own it safely and at scale?”

One useful mental model: Ethereum is closer to a mix of global settlement rails + productive collateral than it is to a single product. That’s why network-effect style thinking shows up so often in valuation research. For example, studies on crypto network value frequently find relationships between adoption/usage and valuation consistent with network effects (often discussed through variants of Metcalfe’s Law). If you want a readable academic reference point, see this paper on network effects in crypto valuation: Peterson (2018) – Metcalfe’s Law as a model for Bitcoin’s value. ETH isn’t BTC, but the “usage ↔ value” idea is part of why settlement networks get priced differently than apps.

Pain point #1: “ETH is undervalued” sounds nice — but undervalued compared to what?

When someone says ETH is undervalued, I immediately ask: by which model? Because ETH doesn’t fit neatly into one simple multiple like a stock.

Here are the valuation frames that actually matter in 2026 — and why each one can point to a different “fair value”:

- 1) Cashflow/fee economy thinking

Ethereum produces fees. Some of that value is “returned” via burn (EIP-1559) and some goes to validators (stakers). This makes ETH feel like an asset with an embedded economic engine.If you’re new to this: EIP-1559 changed Ethereum’s fee mechanics so that the base fee gets burned, which can reduce net issuance during high activity. You can verify burn mechanics and issuance dynamics through well-known tracking dashboards (for example: ultrasound.money). - 2) Network usage / “GDP of the chain”

Instead of asking “what’s the P/E?”, you ask: how much economic activity settles here? Think stablecoin transfer volumes, DEX volumes, tokenized treasury settlement, and onchain lending.This is also where mainstream reports matter. For instance, stablecoin usage has been tracked closely by major payment players, and the idea of stablecoins as payment rails has been covered in industry research like Visa’s stablecoin and onchain analytics content (start here: Visa crypto/stablecoin resources). The point isn’t “Visa pumps ETH” — it’s that settlement is becoming a serious category, not just crypto-native trading. - 3) Monetary premium

ETH isn’t only “used.” It’s held. It’s posted as collateral. It’s staked. That creates a scarcity + utility blend that’s hard to compare with traditional assets.And staking changes investor behavior because it turns “holding ETH” into “holding ETH that can produce yield,” which impacts float, liquidity, and long-term demand. - 4) Global settlement narrative

This is the Tom Lee-style frame: if Ethereum becomes the default base settlement layer (directly or via L2s that still anchor to Ethereum), then the market may start valuing ETH like a critical piece of financial plumbing.That’s not “ETH is a better app chain.” That’s “ETH is closer to rails.” Rails get valued differently.

So when you hear a $60K target, the real question is not “is that number crazy?” It’s: which of these models is winning in institutional minds — and which metrics would prove it?

Pain point #2: Retail watches price; institutions watch flows, custody, and regulation

This is where I see most people get blindsided.

Retail tends to anchor on:

- chart patterns

- social sentiment

- upgrades and hype cycles

Institutions tend to anchor on:

- compliant access (can we buy this within our rules?)

- liquidity (can we enter/exit without moving the market?)

- qualified custody (who holds it, how is it insured, what are the controls?)

- clear treatment of staking/yield (is yield allowed, how is it accounted for, what are the risks?)

- regulatory posture (what’s the legal risk for holding/earning on it?)

And here’s the part people underestimate: those factors can move price faster than “tech progress.”

Because once an asset becomes “ownable” by large pools of capital, the market doesn’t need a new invention to reprice — it just needs easier allocation pathways and fewer career risks for the committee approving the trade.

A simple real-world example: when access improves (regulated products, deeper derivatives markets, better custody standards), institutions don’t show up with fireworks. They show up with:

- small starter allocations

- benchmark-driven rebalancing

- policy-based scaling (“if volatility drops” / “if custody is approved” / “if staking treatment is clear”)

That’s why you’ll sometimes see ETH grind, then gap, then never look back — not because of one magical headline, but because the ownership base changes.

Promise solution: I’ll map Tom Lee’s $60K thesis into checkable drivers (so you can agree or disagree intelligently)

I don’t like price-target content that’s basically just chanting numbers. So here’s how I’m going to handle the $60K claim: turn it into a checklist.

When someone says “ETH to $60K,” I want to know what must be true in the real world. For example:

- What metrics should move? (settlement volume, fee/burn behavior, staking participation, liquidity depth)

- What narratives must win? (ETH as settlement rails, ETH as productive collateral, ETH as institutional-grade asset)

- What risks break the thesis? (fee compression, value capture leaking away from L1, regulation around staking/yield)

- What’s “reasonable” in the nearer term? (why targets like $7K–$9K can be argued without assuming the full $60K outcome)

Here’s the question I want you to hold in your head before we go further: if ETH is going to be priced like global rails, what exactly would you expect to see first — onchain, in institutional behavior, and in market structure?

Because in the next section, I’m going to lay out what Tom Lee actually said at Paris Blockchain Week and translate it into the specific bet he’s making — the kind you can track week by week instead of guessing.

What Tom Lee said at Paris Blockchain Week — and what he’s really betting on

At Paris Blockchain Week, Tom Lee (Fundstrat) didn’t pitch Ethereum like “another L1 that might outperform.” He talked about it like financial infrastructure that’s still being priced like a tech experiment.

The headline bits that caught everyone:

- ETH is “grossly undervalued” (his phrase, repeated in different ways).

- $7K–$9K as a nearer-term target range (the “this cycle can do that” move).

- $60K as the “if Ethereum becomes default settlement for tokenized finance” move.

That last one is what people meme. But the real bet isn’t a number. It’s this:

Ethereum becomes the default settlement network for stablecoin payments + tokenized Treasuries + onchain capital markets… and the market starts valuing ETH like base-layer finance, not like a speculative alt.

If you want to sanity-check that bet, you don’t start with “can ETH hit $60K?” You start with: what kind of value would need to settle on Ethereum rails (directly on L1 or through L2s that still anchor to Ethereum), and does ETH actually capture enough of that value through fees, burn, staking demand, and long-term holding behavior?

Here’s the cleanest way I can explain the $60K thesis without turning it into a cult chant:

If Ethereum becomes the “settlement default” for tokenized dollars and tokenized assets, then ETH starts acting less like a growth coin and more like a hybrid of:

- Settlement collateral (needed across the stack for fees, staking, infrastructure demand).

- A fee economy (usage drives fees; fees + burn change supply dynamics).

- A monetary asset (a premium people pay to hold the “reserve asset” of the most trusted smart-contract settlement layer).

And we’re not guessing whether “tokenized dollars and assets” are real. Stablecoins already behave like a working product, not a demo. Multiple public reports over the past couple years (including BIS-style stablecoin discussions and mainstream payments research) keep pointing to the same thing: stablecoins reduce settlement friction—especially cross-border and after-hours—and that’s exactly the kind of boring, high-volume activity that ends up re-shaping rails.

On the tokenized-asset side, the fastest “real finance” wedge has been tokenized Treasuries and funds. If you track the growth of tokenized T-bills and money-market-like products via public dashboards (RWA analytics has gotten surprisingly good), you’ll notice a pattern: institutions don’t start with tokenized stocks. They start with cash and cash-equivalents. That’s where settlement matters most, and where “onchain” stops being a slogan.

That’s the core of Lee’s bet: settlement eats the world, and Ethereum ends up being the settlement layer that institutions trust to be neutral, resilient, and liquid.

Why $7K–$9K can happen without $60K being guaranteed

This is the part most people miss because they want one clean storyline.

$7K–$9K can be a cycle/flows trade. It doesn’t require the world to fully tokenize finance tomorrow. It just needs:

- Risk-on conditions (liquidity and positioning matter more than people admit).

- Big-money access improving (regulated products, custody comfort, clearer rules).

- A narrative institutions can repeat (stablecoins + tokenization + staking yield).

- Supply dynamics doing their thing (periods of net issuance tightening help… a lot).

$60K is different. That’s not just flows—that’s a structural repricing. It implies Ethereum becomes so embedded in financial plumbing that the market assigns ETH a much bigger “monetary premium” and treats its fee economy like a core utility layer.

So when someone says “Tom Lee said $60K,” I translate it as: he’s betting on Ethereum becoming unavoidable. Not just popular.

The institutional angle: what makes ETH easier to own in 2026 than in prior cycles

When I hear “institutions are listening,” I don’t picture some billionaire watching crypto TikTok. I picture:

- Investment committees that want clean custody, clean reporting, and low headline risk.

- Mandates that require regulated venues/products and documented risk frameworks.

- Rebalancing math (if ETH becomes a benchmarked sleeve, flows can turn mechanical).

In prior cycles, ETH ownership at scale got stuck on basic friction:

- “Where do we custody it?”

- “How do we account for staking?”

- “What’s the regulatory treatment of yield?”

- “What happens if something breaks?”

In 2026, a lot of that plumbing is simply less scary. Liquidity is deeper, derivatives markets are more mature, custody options are more battle-tested, and the playbook for “how to hold digital assets without blowing up your compliance department” is more standardized.

That doesn’t guarantee bullish price action, but it changes the speed at which capital can move when sentiment flips.

The valuation toolbox I use (so we’re not just chanting price targets)

I don’t use one magic model for ETH. I use a small toolbox and look for agreement between signals.

- Fee & burn dynamics What I watch: fee generation, burn, and whether ETH is trending net deflationary or inflationary across different market regimes. If usage rises but fee capture collapses, that matters.

- Settlement value Stablecoin supply and transfer volume, tokenized Treasuries/funds growth, onchain DEX volumes, and “real” payments activity. If the chain is settling more value, I want to see it in the data—not just in announcements.

- L2 reality checkDo L2s increase Ethereum settlement demand (posting data, paying for security) or do they end up capturing the economics while L1 becomes a commodity? The answer changes the entire $60K conversation.

- Comparable networks + “GDP of the chain” thinking I compare Ethereum’s economic activity (fees, settlement, liquidity depth, app revenues) to other smart contract networks and even to traditional payment rails—carefully. Not as a perfect match, but as a sanity check.

- Risk premium Security assumptions, governance risk, regulatory headlines, and competitive threats. ETH can be “useful” and still be priced with a higher risk discount if institutions feel uncertain.

Key catalysts that could make the thesis real in 2026

If you’re trying to spot whether we’re moving from “bull market noise” to “structural repricing,” these are the catalysts I keep coming back to:

- Stablecoin growth + real payments adoption Not just exchange settlement—actual commerce flows, remittances, B2B settlement, payroll experiments. This is where stablecoins stop being “crypto” and start being “finance.”

- Tokenized assets settling on Ethereum rails Tokenized Treasuries are the gateway drug. If more funds, credit products, and settlement layers anchor to Ethereum (even via L2s), that supports the “base-layer finance” story.

- Staking participation + yield perception going mainstream When conservative allocators view staking as “protocol-native yield” rather than “weird crypto interest,” it changes sizing behavior.

- L2 scaling that increases L1 settlement demand Scaling needs to translate into sustainable settlement value for Ethereum—not just cheaper transactions elsewhere. If L2 growth increases blob usage / settlement posting and Ethereum remains the anchor, that’s supportive.

- Macro tailwindsLiquidity conditions still matter. Even the best structural story often needs the market’s permission to re-rate.

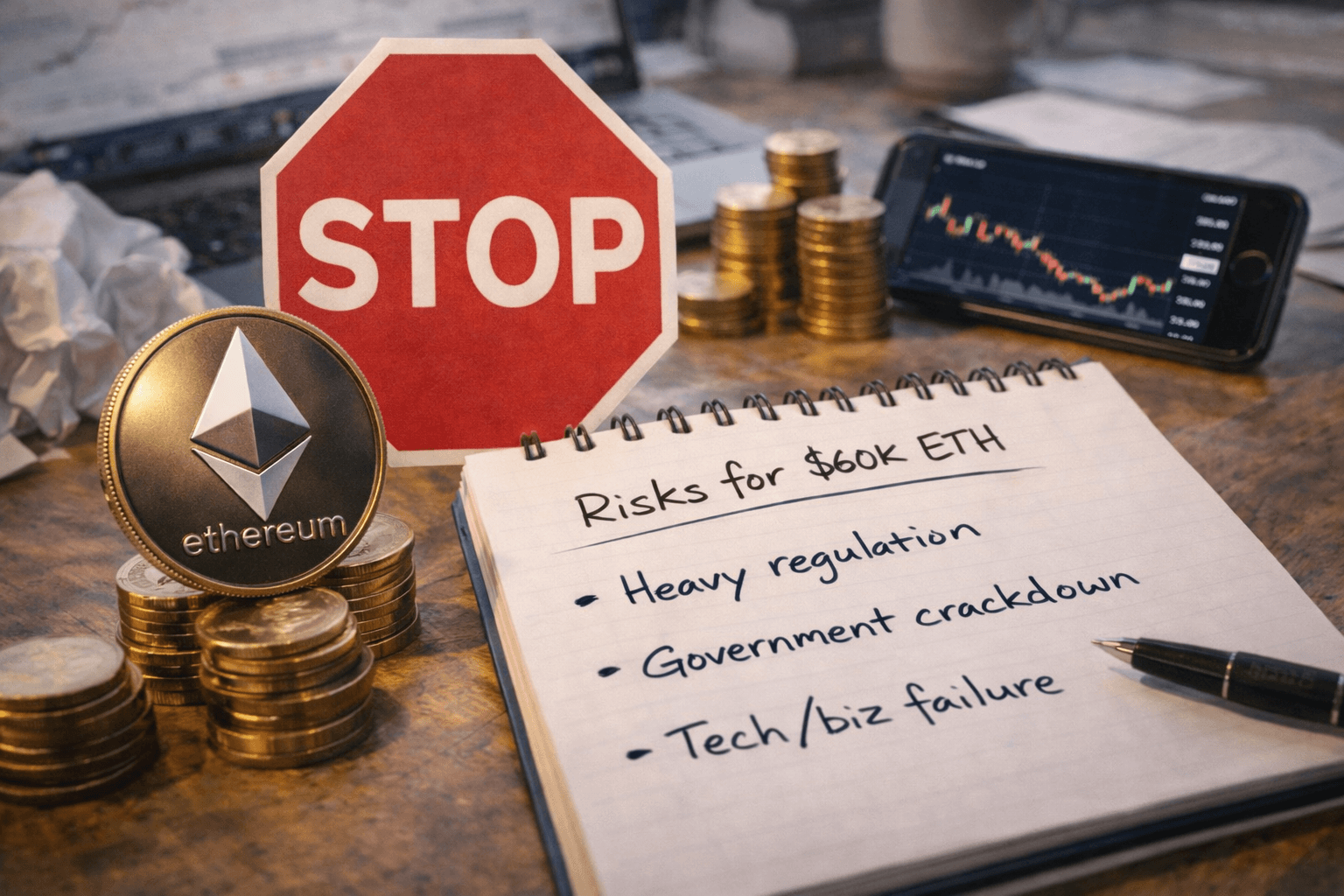

The uncomfortable section: what could stop ETH from reaching $60K

I like upside, but I don’t trust narratives that won’t look at the sharp edges. Here are the real “thesis breakers” I keep on my desk:

- Fee compression + weak value capture If L1 fees structurally compress and Ethereum doesn’t capture enough value from L2 activity, the “fee economy” repricing gets harder.

- Regulation around staking/yield or transaction privacy ETH doesn’t exist in a vacuum. If staking is treated in a way that scares regulated allocators, demand can soften fast.

- Alternative ecosystems win institutional settlement Institutions may choose a different settlement stack if it’s simpler, cheaper, or politically safer—even if Ethereum is more decentralized.

- Security / MEV failures or governance blowups If the market starts to question credible neutrality or execution safety, the monetary premium gets hit.

- Narrative fatigue If “tokenization” stays mostly press releases and pilot programs, price targets like $60K lose oxygen.

People Also Ask (straight answers)

- Can Ethereum really reach $60,000?Yes, in the sense that it’s not physically impossible—crypto reprices violently when a network becomes “default.” But it requires massive settlement adoption and Ethereum maintaining strong value capture (fees/burn/staking demand) even as L2s scale.

- What would Ethereum’s market cap be at $60K?Rough math: price × circulating supply. With supply roughly in the ~120M range (it moves, so check a live tracker), $60K implies about $7.2T. That’s the point: the $60K call is implicitly a claim that Ethereum becomes global financial infrastructure scale.

- Is staking still worth it in 2026? It depends on your goals and constraints. For long-term holders, staking can make sense as a way to earn protocol yield—but you have to weigh lockups/liquidity, smart-contract/platform risk (if liquid staking), and regulatory/tax treatment where you live.

- Does L2 growth help or hurt ETH price? Both are possible. L2 growth helps if it increases Ethereum’s settlement demand and keeps Ethereum as the trusted anchor. It hurts if most economic value stays on L2s while L1 becomes a low-fee commodity with weaker capture. Watching L1 settlement fees + L2 posting costs is key.

- What’s Tom Lee’s track record on crypto calls? He’s been early on some major crypto theses and wrong on timing plenty of times—like most macro-style strategists. I treat his calls as scenario framing more than “precision forecasting.” Useful for building a checklist, dangerous as a blind target.

- What price levels matter: $7K, $9K, $10K, previous ATH? Traders fixate on round numbers, but I care about previous ATH zones (supply overhang), then $7K–$9K as the “institutions can talk about this without sounding crazy” zone, and $10K as a psychological regime shift where positioning often changes.

- What’s the biggest risk to the ETH bull case? The biggest single risk is value capture: adoption happens, activity grows, but ETH doesn’t capture enough of the economic upside because fees compress and alternative layers absorb the margin.

Quick links I’m watching (context, clips, and reactions — not financial advice)

If you want to see how the conversation is moving in real time, here are a few posts I’ve been checking to gauge sentiment, framing, and the “what are people repeating?” effect:

- Cointelegraph clip/post on the $60K ETH talk

- CoinMarketCap reaction thread

- KalshiTrade angle (market-style framing)

- BMNRBullz commentary

- CryptosR_Us take

- conorfkenny thread

- Crypto__Goku reaction

Now here’s the question I think actually matters—and it’s the one I’m going to answer next in a way you can track weekly without guessing:

If ETH is going to re-rate like financial infrastructure, what are the exact signals that tell me we’re in the bull path… versus a normal cycle pump?

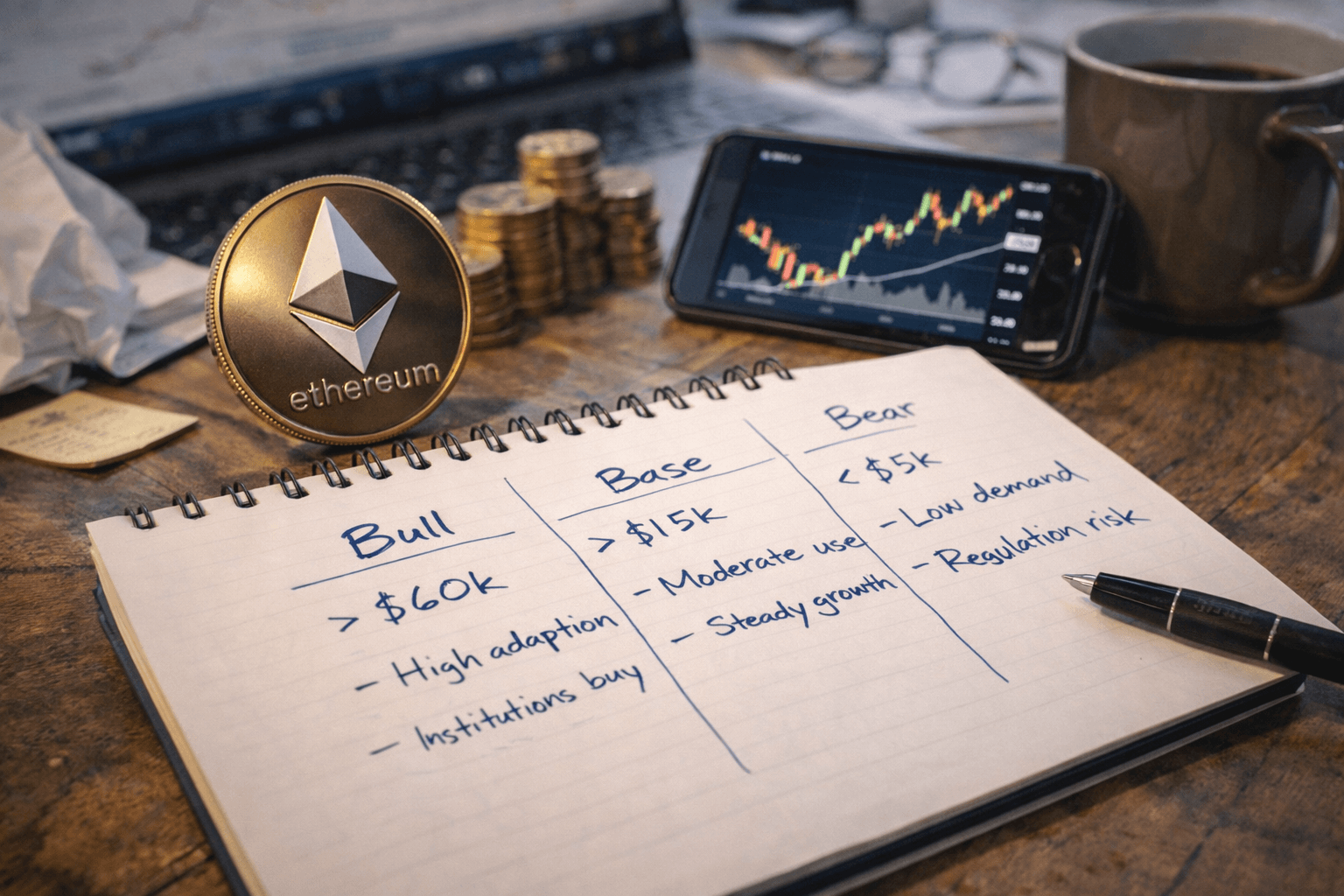

What it means for ETH in 2026: my game plan (bull/base/bear) and how I’d approach it

Tom Lee’s $60K number is flashy, but the useful part is this: it forces you to stop thinking in “price predictions” and start thinking in paths.

When I’m watching ETH, I’m not trying to guess the exact top. I’m asking one boring question that decides everything:

Is Ethereum becoming financial infrastructure and still capturing value while it scales?

Below is how I frame 2026 in three scenarios—each with clear “tells” so I’m not trading vibes.

Bull case: the “global settlement + institutional flows” breakout (how $60K becomes thinkable)

In the bull case, ETH stops trading like “a big crypto asset” and starts getting priced like critical rails:

- Stablecoins and tokenized assets keep expanding on Ethereum-aligned rails (L1 + major L2s), and settlement becomes routine—not a crypto-native novelty.

- ETH value capture holds up even as users live on L2s (meaning L2 scale doesn’t starve the base layer; it feeds it).

- Regulated access + custody makes ETH easy to own at size (funds, RIA models, corporates, pensions via approved wrappers).

- The market assigns a “monetary premium” to ETH because it’s the asset most tied to the settlement layer + collateral + staking security.

Here’s what I’d need to see for $60K to stop sounding like a meme and start sounding like an (aggressive) valuation outcome:

1) Settlement growth that looks like finance, not just trading

If stablecoin activity is mostly exchange churn, it’s fragile. If it’s payroll, remittances, merchant settlement, B2B flows—those habits stick.

I’m watching stablecoin supply and usage on public dashboards like:

- DeFiLlama Stablecoins (supply trends + chains)

- Dune (custom dashboards for payments, bridges, L2 activity)

And yes, I care about “studies” here because this isn’t just crypto hype—traditional institutions are researching this. The BIS has published multiple reports over the last few years highlighting stablecoins’ role in cross-border payments and the risks/requirements for adoption (compliance, reserves, settlement finality). The point isn’t that BIS is bullish; it’s that this is now mainstream plumbing research.

2) Tokenized treasuries / funds don’t stall out

Tokenized real-world assets are one of the cleanest “adult” use cases because they’re boring by design: T-bills, money market funds, credit. We’ve already seen big names experiment here (BlackRock’s BUIDL, Franklin Templeton’s onchain fund initiatives). If that category keeps compounding, Ethereum’s “global settlement” narrative stops being theoretical.

3) ETH still gets paid when L2s win

This is the make-or-break piece. L2s are great for users. For ETH holders, what matters is whether scale routes value back to Ethereum through:

- blob/DA demand and L1 settlement costs,

- security reliance (finality and dispute resolution anchored to L1),

- ETH’s role as the core collateral and staking asset.

If L2 activity explodes but ETH issuance creeps up, burn collapses, and L1 becomes a sleepy courthouse no one pays for, the bull case breaks.

4) Institutions don’t just “buy”—they allocate

There’s a big difference between a few headline purchases and a world where ETH becomes a model portfolio sleeve (with rebalancing rules and benchmarks). That’s where persistent demand comes from.

In this bull scenario, I’d expect to see “boring” behavior:

- consistent inflows via regulated products,

- staking viewed as a standard yield component (with clear tax/accounting treatment),

- ETH treated as strategic exposure rather than a tactical trade.

What it looks like on the chart (without pretending TA is magic)

If ETH is truly re-rating, it tends to reclaim major levels and then behave differently around them: less violent give-back, quicker bid on dips, and better performance during risk-off weeks. That’s not a guarantee—just a common “feel” of structural demand replacing tourist liquidity.

Base case: ETH wins, but pricing is slower and choppier than the headline

This is honestly the scenario I plan around most, because it fits how markets usually work: messy, political, and full of fake-outs.

In the base case:

- Ethereum remains the default smart contract settlement layer for serious capital,

- L2s keep scaling user activity,

- institutions keep coming—but in waves, not a straight line,

- ETH can absolutely tag major milestone zones like $7K–$9K in a strong cycle.

But $60K needs either:

- a longer runway of adoption (multi-year compounding of settlement + tokenization),

- or a stronger macro backdrop (liquidity + risk appetite),

- or clearer proof that Ethereum captures fees/security premium even as execution migrates to L2s.

What base-case “tells” look like:

- healthy, not euphoric growth in stablecoin supply and RWA activity,

- L2 growth without a matching collapse in Ethereum’s economic relevance,

- fee/burn cycles that fluctuate but don’t flatline for months,

- periodic institution-led bids followed by frustrating consolidations.

If you’ve been in crypto a while, you know this movie: everyone wants a clean “up only” thesis, but the market makes you earn it by chopping your patience in half.

Bear case: adoption grows but ETH doesn’t capture enough value (or regulation clamps down)

This is the one people wave away too quickly. The bear case isn’t “Ethereum dies.” It’s nastier:

Ethereum succeeds… and ETH underperforms anyway.

How does that happen?

- Fee compression: users move to cheap environments, and the base layer doesn’t get enough high-value settlement to compensate.

- Value capture leakage: MEV, sequencer economics, app-chains, or alternative DA models siphon away what people assumed would accrue to ETH.

- Regulatory hits: staking/yield treatment becomes toxic for certain institutions, or compliance rules reduce who can touch yield-bearing ETH products.

- Institutional settlement goes elsewhere: a rival stack becomes the “approved” choice for big distribution, even if Ethereum stays the most used by crypto natives.

Bear-case “tells” I take seriously:

- stablecoins and RWAs grow, but not on Ethereum-aligned rails,

- L2s flourish while L1 economics trend weaker over long windows,

- staking participation drops or centralizes uncomfortably,

- major compliance narratives turn against permissionless settlement.

This is also where “narrative fatigue” matters: if adoption headlines keep coming but price can’t respond for months, eventually even strong communities lose attention—and attention is liquidity in crypto.

Practical checklist: what I’m tracking weekly (so this isn’t just storytelling)

I keep this simple. Weekly means: signals, not minute-by-minute noise.

1) Price levels that actually matter

- prior cycle ATH zones (market memory is real)

- psychological levels ($5K, $7K, $10K style areas)

- ETH/BTC trend (if ETH can’t hold up here, the “re-rating” story weakens)

2) Net issuance, burn, and “is ETH acting like a scarce asset?”

- I check ultrasound.money for issuance/burn dynamics.

- I’m not looking for one hot week. I’m looking for multi-month regimes: is ETH structurally tight, or structurally inflating?

3) L1 vs L2 economics (the value-capture reality check)

- L2 activity and rollup landscape via L2BEAT

- What I want: L2s growing and evidence that Ethereum remains the paid settlement layer (not just the forgotten judge)

4) Stablecoin settlement + where it’s happening

- chain share shifts (are Ethereum and its major L2s gaining or losing?)

- usage composition (payments-like behavior vs exchange churn)

5) Staking participation and concentration

- staking ratio trend (steady is fine; chaotic swings aren’t)

- validator/custodian concentration (centralization risk shows up slowly, then all at once)

- basic validator stats via explorers and staking dashboards (e.g., beaconcha.in)

6) Flows and “can big money buy this cleanly?”

- regulated product flows (when available)

- liquidity depth on major venues

- custody/prime brokerage headlines (this stuff moves slower than Twitter, but faster than people think)

7) Regulatory headlines that actually change behavior

- staking/yield guidance

- stablecoin frameworks

- privacy/AML enforcement direction

My rule: I don’t react to “noise.” I react when something changes the incentives for large allocators or breaks the economics of settlement.

Closing thought: don’t argue the number first—argue the path

I’m not married to $60K. I’m married to a framework that keeps me honest.

If Ethereum becomes the place where stablecoins, tokenized treasuries, funds, and onchain credit routinely settle, and ETH continues to capture value as the secured asset behind that system, then extreme targets stop sounding extreme surprisingly fast.

If that path doesn’t materialize—if value capture leaks away, or regulation blocks the clean institutional trade—then $60K will age like a headline, not a forecast.

The best way to think about Tom Lee’s call is not “is $60K crazy?” It’s: “is Ethereum becoming financial infrastructure, and does ETH still get paid if it does?”

That’s the game plan I’m running in 2026: watch adoption, watch value capture, and let the price targets be the output—not the thesis.