Morgan Stanley’s 0.14% $MSBT Bitcoin ETF Goes Live This Week — Here’s What $6T in Advisor Assets Could Mean for BTC Flows in 2026

What happens when Bitcoin demand doesn’t show up as a loud green candle… but as a quiet checkbox inside a wealth manager’s “approved products” list?

That’s why I’m paying attention to Morgan Stanley potentially rolling out a 0.14% spot Bitcoin ETF ($MSBT) with access through a channel of roughly 16,000 advisors. If this goes live on April 8, 2026, it’s not just “another ETF.” It’s a distribution machine switching on—aimed at clients who usually move slower… but when they move, they move big.

And yes, I know the internet loves to label every headline “institutional adoption.” Most of the time that phrase is misunderstood.

The problem: most people misunderstand what “institutional adoption” actually looks like

Retail traders often picture institutions arriving like this:

“One day they all buy at once and Bitcoin instantly rips.”

In real life, the money that matters often enters in a boring way—through processes that are designed to be boring:

- Portfolio policy updates (what’s allowed, what’s not)

- Compliance guardrails (position limits, suitability, risk disclosures)

- Model portfolio allocations (1% here, 2% there—then rebalanced)

- Slow rebalancing flows (monthly/quarterly, sometimes tied to new deposits)

If you’ve watched how ETF adoption played out in other markets, you’ve seen this movie. The earliest phase rarely looks dramatic—until you zoom out and notice the steady “drip” became a consistent stream.

A useful comparison is the broader ETF industry itself: when ETFs became the default wrapper for stock and bond exposure, the shift didn’t happen in one day. It happened because ETFs made allocation, reporting, and rebalancing easier, and advisors could implement them at scale. This is also why research from groups like the Investment Company Institute (ICI) has long highlighted how ETFs fit into long-term portfolio construction rather than short-term trading behavior.

So if a wirehouse channel makes Bitcoin exposure “normal” inside the system, the adoption signal won’t be a meme trend. It’ll be a set of small, repeatable flows.

Why the fee number matters more than it sounds (0.14% is a weapon)

A 0.14% expense ratio doesn’t sound exciting until you realize what it actually does in the ETF world: it pressures every competing product sitting next to it on a platform menu.

Fees aren’t just marketing. They’re a message:

- “We plan to win flows.”

- “We expect this to be held long-term.”

- “We want to be the default pick in model portfolios.”

In spot Bitcoin ETFs, even small fee differences can matter because many investors treat them as commodity-like exposure. If two funds are both spot-based and both liquid, the cheapest option starts to look like the “sensible” option—especially to advisors who don’t want to justify why they picked a higher-cost wrapper.

And here’s the part most people miss: a low-fee launch doesn’t only attract new buyers. It can also pull assets from existing ETFs through switching. That’s not theory—this pattern shows up across ETF categories whenever a cheaper, credible issuer enters and the wrapper is largely interchangeable.

If $MSBT truly hits the market at 0.14%, it’s basically Morgan Stanley saying: “We’re not testing demand. We’re trying to own the lane.”

The real “pain point” for wealthy clients: access + simplicity + reporting

I’ve talked to enough long-time investors to know something important: plenty of high-net-worth clients don’t avoid Bitcoin because they “don’t get it.” They avoid it because the implementation is annoying, messy, or hard to fit into their existing financial life.

An ETF wrapper solves problems that matter a lot more to wealthy households than crypto Twitter likes to admit:

- Clean tax documents (a familiar 1099 flow instead of crypto exchange exports)

- Brokerage custody inside accounts they already use

- Simple position sizing (a 0.5% sleeve is just a trade, not a new custody setup)

- Consolidated reporting for estate planning and household balance sheets

It’s the same reason many investors buy gold exposure through ETFs instead of storing bars. Not because they hate the asset—because they want the convenience of the wrapper.

And convenience is powerful. In finance, the product that fits into existing workflows often wins—even if the underlying asset is the same.

Promise solution: how I’ll estimate what $MSBT could do to BTC demand in 2026

I’m not going to pretend we can predict exact inflows from day one. Anyone promising a precise number is guessing.

What I can do is map realistic scenarios based on how advisor channels actually behave. In the next section, I’ll build a simple framework with:

- Conservative / base / aggressive adoption paths

- The assumptions that actually move the needle (and the ones that don’t)

- What to watch week-by-week after launch so you don’t get fooled by headlines

Because here’s the real question you should be asking right now:

If Morgan Stanley’s advisor network controls trillions in client assets, what does even a tiny allocation to a spot Bitcoin ETF look like in actual dollar flows—and how fast would it show up?

Let’s quantify that next—and separate “big name launch” hype from the numbers that could really move the market.

What’s actually different about Morgan Stanley launching the cheapest spot BTC ETF

If the rumored 0.14% spot Bitcoin ETF ($MSBT) goes live, the “cheap fee” headline will get all the attention. But the real edge isn’t the basis points — it’s the distribution engine behind them.

Morgan Stanley doesn’t need to win Crypto Twitter. It needs to win:

- model portfolios (where defaults quietly become destiny)

- discretionary managed accounts (where small sleeves get deployed at scale)

- strategic allocation buckets (where “1% here” can be billions)

A “cheapest in class” ETF is often a land-grab strategy. In ETF history, low fees tend to concentrate assets into a few winners because advisors and platforms prefer simple, repeatable choices. Vanguard built an empire on that behavior in plain-vanilla indexing — and the same psychology shows up whenever a category matures.

In wealth management, the product that becomes the default option doesn’t need hype. It needs approvals, shelf space, and a fee nobody has to defend.

Also, a small but important note: with spot Bitcoin ETFs, fee competition isn’t just marketing. It affects how comfortable an advisor feels putting it into a long-term sleeve without getting the “why is this so expensive?” question every review meeting.

Advisor distribution 101: why 16,000 advisors beats “crypto Twitter hype”

Here’s how the real world works: most client money doesn’t “YOLO in.” It moves through model portfolios, Investment Policy Statements (IPS), and platform-approved lists.

When a product is approved inside a major advisor network, it can turn into the default answer to a simple client question:

“Can we add a little Bitcoin exposure without making my taxes and reporting a nightmare?”

That matters because advisors influence flows in three powerful ways:

- They standardize behavior. If the “house view” is a 0.5%–1% sleeve for certain risk profiles, it gets replicated again and again.

- They implement gradually but persistently. Rebalances, new deposits, and periodic reviews create a steady bid, not a one-day spike.

- They reduce friction. The moment something becomes “approved,” a huge chunk of hesitation disappears — not because clients suddenly love Bitcoin, but because the process becomes normal.

And this isn’t just theory. Research on ETF ecosystem mechanics repeatedly shows that flows (not noise, not volume) are what can push underlying markets around. For example, academic work like Ben-David, Franzoni & Moussawi (2018) links higher ETF ownership and the creation/redemption mechanism to changes in volatility and return dynamics in underlying assets — the point being: ETF plumbing can become market structure once the vehicle is widely used.

The $6T question: what percentage matters, and why

When people throw around “$6 trillion in advisor assets,” it can sound too big to be useful. So I keep it simple: the only number that matters is the allocation percentage that actually sticks.

Here’s the clean math framework (not a prediction, just a lens):

- 0.25% of $6T = $15 billion

- 0.50% of $6T = $30 billion

- 1.00% of $6T = $60 billion

Now the reality check: those dollars don’t land in one afternoon candle.

Advisor allocations typically “ladder” in through:

- scheduled rebalances (monthly/quarterly is common)

- new cash flows (payroll liquidity, business sales, inheritances, distributions)

- risk-on windows (when clients feel brave and headlines aren’t scary)

- model updates (slow to change, but sticky once they do)

So if you’re looking for a single “launch week” number to confirm the thesis, you’ll probably miss what’s actually happening. The tell is whether flows show up consistently after the initial excitement fades.

The “ETF plumbing” readers should understand (this is where flows become real)

Spot Bitcoin ETFs aren’t magic wrappers. They’re machines with a very specific mechanism that connects demand for shares to demand for actual BTC.

Here’s the simplified version:

- Authorized Participants (APs) create or redeem ETF shares based on supply/demand.

- When there’s net inflow, APs deliver cash (or sometimes BTC, depending on structure) to the fund.

- The fund (through its execution partners) sources spot Bitcoin and holds it with a custodian.

- This is why net inflows matter more than trading volume: volume can be traders swapping shares back and forth; net inflow is what forces the machine to buy.

If you want to track what’s real, watch:

- daily net creations/redemptions (not just price action)

- AUM growth (is it compounding or stalling?)

- premium/discount behavior (does the arbitrage mechanism look healthy?)

- spreads and liquidity (tight spreads attract allocator usage)

This is also where I like to keep one mental guardrail: big volume days don’t automatically mean big BTC buying days. Volume is emotion. Flows are commitment.

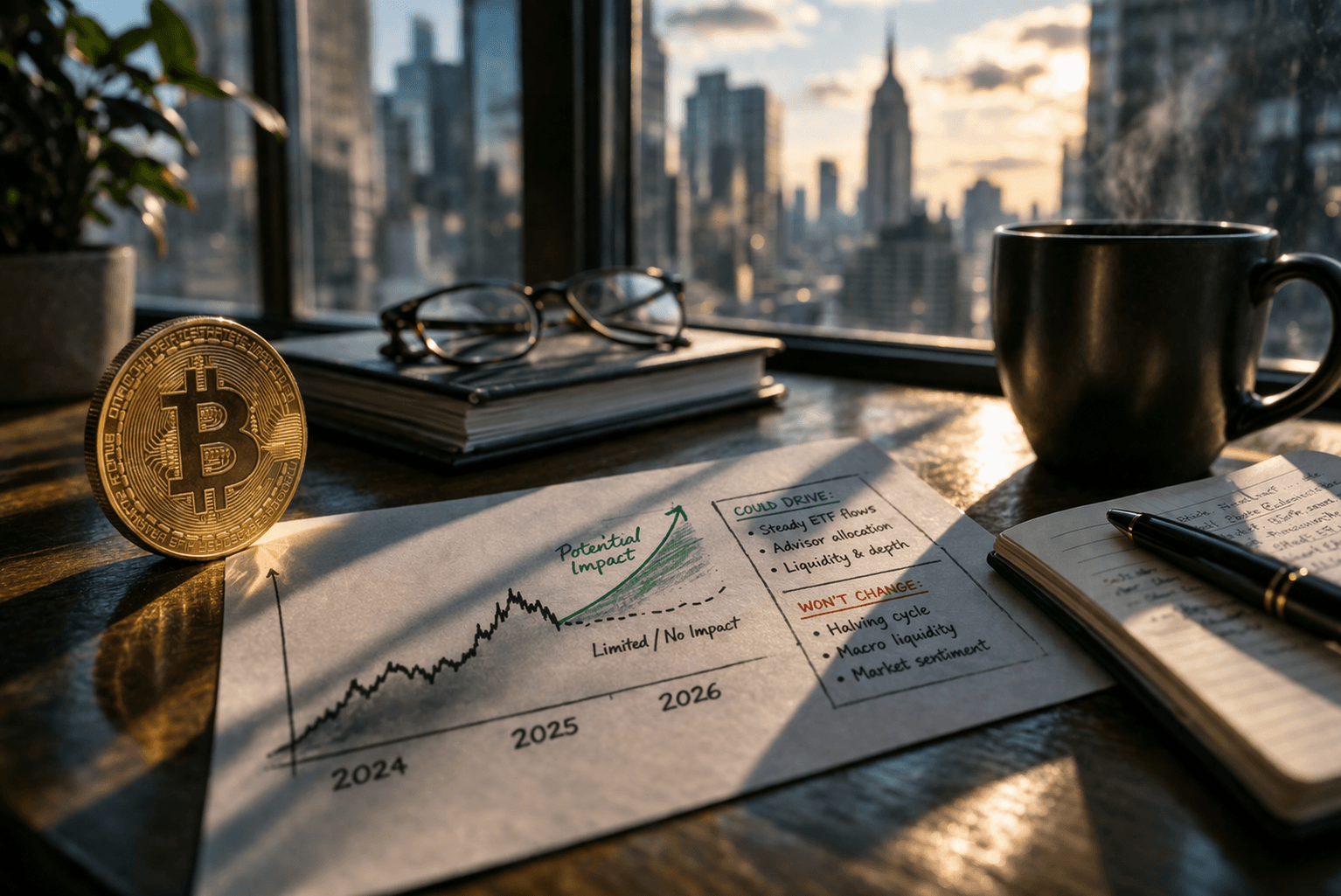

What $MSBT could change for BTC price action in 2026 (and what it won’t)

If $MSBT gets meaningful advisor adoption, it can change how dips behave.

I’m not saying “flows guarantee up-only.” Macro liquidity, equities risk appetite, rate expectations, and profit-taking still run the show. But sustained ETF inflows can create something Bitcoin historically hasn’t always had at scale:

a steadier institutional bid underneath the market — especially during pullbacks when models rebalance.

What it won’t do:

- It won’t eliminate volatility.

- It won’t prevent drawdowns during broad risk-off events.

- It won’t stop long-term holders and miners from selling into strength.

What it can do is change the shape of demand from “burst and fade” to “drip and accumulate” — and markets tend to respect persistent buyers.

A simple 3-scenario flow model I’ll use (conservative / base / aggressive)

When I model potential impact, I don’t start with hype. I start with four knobs that actually move numbers:

- adoption rate inside advisor books (how many advisors use it at all)

- allocation size per client sleeve (0.25%, 0.5%, 1% is the real battlefield)

- rebalance cadence (monthly vs quarterly changes speed dramatically)

- competitive response (fee cuts, waivers, platform placement)

Then I sanity-check each scenario like an advisor would:

- Conservative: narrow adoption, tiny sleeves, slow rebalances, strong competitor defense.

- Base: moderate adoption, 0.25%–0.50% sleeves, quarterly implementation, mild fee war.

- Aggressive: fast approvals + model inclusion, 0.50%–1.00% sleeves for risk-on profiles, persistent inflows.

The key is this: implementation speed can matter as much as total dollars. $15B over 3 years is not the same market impact as $15B over 3 months.

The second-order effects: fee wars, ETF consolidation, and “default winners”

The moment a major brand tries to anchor the category at 0.14%, competitors have choices — none of them fun:

- Cut fees (and admit they were overcharging, or eat margin)

- Offer temporary waivers (good for headlines, but watch what happens when waivers end)

- Fight for platform placement (wirehouses and custodians can “guide” flows without banning anyone)

- Merge/close smaller funds (ETF history is full of “zombie funds” that eventually get shut down)

In many ETF categories, assets concentrate into a handful of “default winners” because advisors and institutions value:

- tight spreads

- deep liquidity

- brand and operational comfort

- fees that don’t raise eyebrows

If $MSBT truly lands as the cheapest option with strong distribution, it doesn’t just bring new buyers — it can trigger switching from existing spot BTC ETFs too. That switching still matters because it can reshuffle liquidity leadership and accelerate the “winner-take-most” dynamic.

What people also ask (and what I’ll answer clearly)

“Is a 0.14% Bitcoin ETF actually safe?”

Fee level doesn’t equal safety. “Safe” here really means: how clean is the structure, custody, and operational setup?

What I check (and what you should check in the prospectus/filings):

- Custodian details: Who holds the BTC? How is it stored (cold storage policies)?

- Insurance language: Is it real coverage or vague marketing? What are exclusions?

- Counterparty risk: Which entities are involved in execution, financing, and custody operations?

- Disclosure clarity: Do they explain forks, airdrops, and how extraordinary events are handled?

Most investors underestimate this: the biggest “ETF risk” usually isn’t that the price won’t track — it’s operational and legal edge-cases you only see when something breaks.

“Will advisors really recommend Bitcoin now?”

Most advisors won’t “recommend Bitcoin” the way the internet says it. In practice, it’s more like:

“For certain clients, we can allow a small allocation sleeve to a spot BTC ETF within defined risk limits.”

Advisors work inside suitability rules and compliance guardrails. That means:

- risk profiling matters (time horizon, drawdown tolerance, liquidity needs)

- position sizing matters (small sleeves are easier to defend and monitor)

- documentation matters (IPS language and review notes)

So yes, adoption can happen — but it often looks boring, controlled, and gradual.

“Does an ETF buy real Bitcoin or just track the price?”

A spot Bitcoin ETF is designed to hold actual BTC (through its custody arrangement) to back shares. That’s different from futures-based products, which use derivatives and can behave differently due to roll costs and futures curve structure.

If you want to confirm the “real BTC” part, look for:

- daily holdings reporting (many spot ETFs publish BTC held)

- creation/redemption language in disclosures

- custody disclosures naming the custodian and storage practices

“How soon would institutional flows show up after launch?”

Not instantly. There’s usually a sequence:

- platform onboarding (availability across advisor systems)

- internal approval lists (what’s permitted, under what conditions)

- model portfolio updates (slow, but powerful)

- first rebalance window (often when you see the “real” start)

There’s also a difference between:

- announcement-driven trading (fast, emotional, often fades)

- allocation-driven buying (slower, repetitive, tends to persist)

If you’re trying to time it, watch weeks 2–8 more than day 1.

The early signals I’m watching in week 1–4 after launch

If $MSBT is real and live, I’m not going to get distracted by headlines. I’m watching a checklist that answers one question: is this becoming a default allocation tool, or just a news-cycle event?

- Daily net flows: are inflows consistent, or one-and-done?

- AUM trajectory: does it stair-step higher each week?

- Liquidity/spreads: are spreads tight enough for advisors to use without client complaints?

- Premium/discount stability: does ETF plumbing look smooth?

- Custody partner notes: any meaningful operational disclosures?

- Platform availability: can advisors actually buy it across internal systems?

- Competitor response: fee cuts, waivers, sudden “promo” pushes

And one practical tip: I compare $MSBT’s early flow pattern to how other major spot BTC ETFs behaved in their first month. Not because history repeats perfectly — but because distribution-driven ETFs tend to show a more durable flow signature than hype-driven ones.

Quick resources I’m tracking on this $MSBT launch

These are starting points I’m watching for chatter, screenshots, and claims — and I verify anything important against official filings and statements before treating it as fact:

- https://x.com/ItsBitcoinWorld/status/2041513155680141406

- https://x.com/coinlore/status/2041594238090039390

- https://x.com/crediful/status/2041565185354113457

- https://x.com/Shravjhangiani/status/2041527107587539062

- https://x.com/sea_pegasus/status/2041801655730237453

- https://x.com/bsc_daily/status/2041802372440068361

- https://x.com/TKVResearch/status/2041795757112799561

- https://x.com/Bitcoindiy/status/2041800261895692439

- https://x.com/Btc_MindShifts/status/2041591650854826424

Now for the part most people get wrong: even if the ETF is “successful,” it might not mean net-new demand for Bitcoin… it could be a massive rotation from other ETFs.

So how do I tell the difference between switching flows and true incremental demand — and what does that change about my 2026 BTC outlook?

I’m going to answer that next, with a blunt tracking playbook and the few risks that can quietly kill the whole “advisor adoption” narrative without anyone noticing.

What this likely means for BTC institutional flows in 2026 (my honest take)

If the two claims hold up in the real world — 0.14% fees and real advisor distribution — then $MSBT isn’t just “another spot Bitcoin ETF.” It’s a routing change for where Bitcoin exposure gets sourced inside wealth management.

Here’s the part most people miss: the first wave probably won’t look like a sudden tsunami of brand-new Bitcoin buyers. It’ll look like quiet switching and default selection.

Switching, because fees matter more than people want to admit. Morningstar has published versions of the same conclusion for years: lower-cost funds tend to gather more assets, and fees are one of the most consistent predictors of which products “win” flows over time. Not because investors are fee-obsessed — but because platforms, models, and committees can justify “cheapest credible option” without taking career risk.

Default selection, because a house-approved ETF becomes the easy answer. In advisory land, “We can use the firm’s preferred product” is often the difference between an allocation happening this quarter… or never.

So when I think about 2026, I’m watching for two separate effects:

- Net-new Bitcoin demand from clients who were waiting for a familiar wrapper and an advisor-friendly green light.

- Asset migration from other spot BTC ETFs into the lowest-fee, easiest-to-approve option (especially inside managed accounts and model portfolios).

That second bucket won’t show up as “Bitcoin adoption exploded” on social media, but it can still reshape the ETF leaderboard fast — and it can still matter for price if the net flows stay positive while supply is tight.

If you want a real-world analogy, I always think about the gold ETF era. When SPDR Gold Shares (GLD) launched, a lot of the story wasn’t “humans discovered gold.” It was “gold got a frictionless wrapper,” and that wrapper pulled demand forward. Researchers have studied how easier access via ETPs changes participation and flow dynamics in commodities. Bitcoin’s version is playing out in public, just at internet speed and with sharper narrative swings.

My practical playbook: how I’d track $MSBT impact without guessing

I’m not going to pretend I can forecast the exact number of coins this thing “must buy.” What I can do is track the few boring signals that consistently separate headline noise from real allocation behavior.

Here’s exactly how I’d follow $MSBT week-by-week without turning it into a guessing game:

- Track daily and weekly net inflows (not volume)

Volume is often traders swapping shares back and forth. I care about whether the fund is growing or just being day-traded.

Practical tip: I usually cross-check numbers against at least two sources (issuer updates + a third-party tracker). For Bitcoin ETF flow dashboards, people often use public aggregators like Farside as a starting point, then verify with the fund’s own reporting. - Watch AUM “stickiness” after the first hype week

Week 1 can be promotional, curiosity, or short-term positioning. The signal is whether AUM keeps stair-stepping higher in weeks 2–6 — especially during boring, sideways markets. - Look for advisor-platform availability and internal adoption breadcrumbs

I’m looking for signs like:- platform access expanding (which custodial platforms / account types can buy it)

- research notes or “approved list” mentions

- model portfolio inclusion (even as a small sleeve)

- training webinars and compliance guidance becoming standardized

When advisors start hearing “yes, you can use it” more than “not yet,” the flow profile changes.

- Compare competitor fee changes and waivers in real time

The easiest tell that $MSBT is hitting nerves is watching what rivals do next. If you see:- fee cuts

- temporary waivers

- platform promotions

- marketing pushes aimed specifically at advisors

…that’s not random. That’s defense.

- Confirm spot holdings transparency and custody details

I want clean, routine disclosure: holdings updates, clear custody arrangements, and no weird gaps where you have to “trust the vibes.” If holdings reporting is delayed, inconsistent, or overly vague, I downgrade my confidence quickly. - Separate headline pumps from allocation flows

The market loves a dramatic storyline. But allocation flows have a different fingerprint: they show up as steady inflows over time, often clustering around typical rebalance windows, and they tend to persist even when Bitcoin isn’t trending on X for 48 hours.

If you want a simple rule: price can lie for weeks; flows are harder to fake.

Key risks and speed bumps people ignore

This is the part where I try to keep myself honest. Even if $MSBT is real, cheap, and widely distributed, there are still very normal reasons flows could come in slower than the headlines imply.

- Compliance friction can slow everything down

Advisors don’t just “like Bitcoin” and click buy. There’s suitability, documentation, risk profiles, and sometimes product-specific rules. A product can exist and still be practically unavailable in certain account types for months. - Risk-off macro can freeze new allocations

If markets go into a defensive regime (rates, recession fears, equity drawdowns), advisors often shift into capital preservation mode. Bitcoin exposure becomes “review later,” even if the product is approved and cheap. - Fee waivers ending can change the story

If any part of the low-fee strategy relies on temporary waivers, the long-term competitiveness depends on what the fee looks like after the promo period. Advisors notice when a “permanent” advantage quietly turns into “intro pricing.” - Tracking, liquidity, or operational hiccups

Even small issues — wider-than-expected spreads, inconsistent premiums/discounts, delayed holdings updates — can keep cautious allocators on the sidelines. Advisors hate explaining “why this product trades weird” to a client. - Rotation risk: flows that look big but aren’t net-new

This is the most misunderstood one. $MSBT could post strong inflows while the category sees muted net growth because money is simply migrating from other spot BTC ETFs. That still matters competitively, but it’s not the same thing as “fresh institutional demand hit the market.”

My baseline expectation is pretty simple: if flows come, they’ll probably come in stages. First the early adopters and self-directed clients. Then the “allowed, but small” sleeves. Then, if Bitcoin behaves (and the world cooperates), gradual model inclusion and bigger wallet share.

The takeaway I’m operating on

The big story here isn’t that Bitcoin got a new ticker.

The big story is that Bitcoin exposure may be turning into a standard portfolio sleeve inside a major advisor ecosystem — the kind of place where money moves slower, but it moves with routines, policies, and repeatable allocation behavior.

So that’s what I’m going to follow: the boring numbers.

AUM growth.Net flows.Platform availability.Fee responses. And whether the adoption curve looks like a one-week marketing event… or a 12-month habit forming.

If you want to track it the same way I do, ignore the loud takes and keep your eyes on the data. I’ll be watching the flow prints and the adoption breadcrumbs closely, because this is one of those moments where the most important signals don’t trend — they accumulate.