Fannie Mae Just Greenlit $4.3T in Crypto-Backed Mortgages — What It Means for Homebuyers in 2026 (and How to Prepare in the Next 12 Months)

What if your Bitcoin could help you qualify for a mortgage… without you having to sell it first?

If you’ve ever stared at your crypto portfolio and thought, “This is worth real money — why does a mortgage underwriter treat it like it doesn’t exist?”, today is a turning point.

Watching your crypto stack grow while a mortgage underwriter acts like it’s Monopoly money has been one of the most aggravating parts of trying to buy a home in the U.S.—especially when rates are high, cash is tight, and every “prove your funds” request feels like a trap that nudges you into selling at the worst possible time and eating a tax bill right before closing. That’s why Fannie Mae’s shift matters: it signals the start of a real, standardized path where major crypto holdings can finally be recognized inside the same system that influences trillions in mortgages, instead of being dismissed as “too hard to verify” or “too volatile to count.” This doesn’t mean instant approvals or that you can wave a wallet and get keys, but it does mean the rules are about to get a lot less random—and if you get your paperwork, custody setup, and timing right over the next 12 months, you’ll be in position to use your crypto strength without panic-selling just to satisfy an outdated checklist.

The conversation just got a lot more serious: Fannie Mae’s mortgage machine — roughly $4.3T in influence across the U.S. housing finance system — has effectively opened the door to crypto-backed mortgage frameworks. Not just for whales and funds. For normal buyers with normal jobs who happened to stack BTC (or other major crypto) early.

Listen to this article:

I’m going to explain this like I would to a friend over coffee: what changed, why it matters for your approval odds, and what you can do in the next 12 months so you’re ready when lenders start rolling this out in the real world.

The real pain: homebuying is already hard — and crypto holders had it worse

Homebuying in the U.S. has been brutal even if you’re doing everything “right.” Rates have stayed high compared to the easy-money era, underwriting is tight, and down payments + closing costs can feel like a second mortgage before you even get the first one.

And if you’re a crypto holder? You didn’t just have the same problems. You got extra ones layered on top.

Here’s what I’ve watched happen to real people over and over:

- They had plenty of assets (sometimes six figures in BTC/ETH)… but underwriters treated it as “not usable.”

- They were pushed to liquidate just to “prove funds,” turning a strong financial position into a tax event.

- They got punished for being early — because the system didn’t have clean rules for on-chain ownership and custody.

And all of this happened while the market was already tough. If you needed motivation to feel frustrated, you didn’t have to look far.

“I can show you my wallet on-chain, I can show you my exchange history, I can show you everything — but the bank still wants me to sell.”

That “sell it” part is where things got expensive fast.

For context, the IRS still treats crypto as property, which means selling can trigger capital gains taxes. This isn’t niche trivia — it’s the kind of surprise that can wreck a down payment plan if you didn’t set aside cash for taxes. (If you want the official word, it’s straight from the IRS here: IRS guidance on digital assets.)

The two big problems crypto buyers kept running into

Most crypto-homebuyer stories boil down to two recurring roadblocks.

1) “Prove your funds” without selling (and triggering taxes)

Mortgage underwriting loves boring money. Payroll deposits. Seasoned cash in a bank account. Predictable paper trails.

Crypto often looked like the opposite — not because it’s illegal, but because the documentation process was inconsistent. A buyer could have $150,000 in BTC sitting untouched for years… and still get asked to convert it to USD and park it in a bank for a certain period just to make it “count.”

That’s where the pain hit:

- Sell crypto → realize gains → owe taxes

- Sell during a dip → lock in losses you didn’t want

- Move funds around → trigger extra questions and delays

Real-world style example: someone bought BTC years ago, it 10x’d, and now they want to use part of it for a home. The lender says, “Great — sell it and show us the cash.” That sale could create a tax bill that wasn’t budgeted, forcing the buyer to either shrink their down payment or pause the purchase entirely.

2) Volatility + custody worries (lenders hate price swings and unclear ownership)

Lenders aren’t built for assets that can move 5–10% in a week. They’re also not built for “trust me, I own it” proof.

Even though on-chain data is public, traditional underwriting systems weren’t designed to interpret:

- self-custody wallets

- token transfers between addresses

- exchange-to-wallet movement

- proof you control the wallet (not just that it exists)

So crypto holders often got lumped into a risk bucket that didn’t match reality: “hard to verify” + “too volatile.” That combination makes underwriters nervous, and nervous underwriters say no.

And yes, volatility is real. Multiple academic and industry analyses have documented crypto’s higher volatility versus traditional assets (which is exactly why lenders historically discounted it or ignored it). If you’ve lived through even one BTC cycle, you already know the story without needing a chart.

Promise solution: what this policy shift unlocks for normal buyers

This is why the Fannie Mae shift matters. It’s not just another headline that makes X scream for 24 hours.

When Fannie’s ecosystem starts recognizing crypto in a more structured way, the practical upside for regular buyers looks like this:

- New paths to qualify where crypto isn’t automatically treated as “unusable.”

- A chance to use crypto without instantly cashing out (which can mean avoiding a forced tax event right before closing).

- Clearer documentation expectations instead of random lender-by-lender “we don’t know, so no” decisions.

- A more mainstream process that plugs into a Fannie framework, not just niche “crypto mortgage” shops with one-off rules.

Let me be very clear: this doesn’t mean you’ll walk into a bank, flash a Ledger, and walk out with a 30-year fixed by lunch.

But it does mean the industry now has a reason to build repeatable rules for something it used to ignore. That’s the difference between a gimmick and a real pipeline.

What this article will answer (based on what people keep asking)

Every time a crypto-and-housing headline pops off, the same questions flood my inbox and search engines. So I’m going to address them head-on in a way that’s actually useful (not hype, not doom).

Here’s what I’m going to answer next, using the same style as those Google “People Also Ask” boxes:

- Can I use Bitcoin to buy a house?

- Do I have to sell my crypto?

- Will this raise my mortgage rate?

- What coins count?

- How do lenders verify crypto?

- What if Bitcoin drops right before closing?

- Is this available now or later in 2026?

And here’s the question that really matters: if lenders start accepting crypto in a Fannie-friendly way, what will they actually require from you — and what moves should you make right now so you don’t get stuck scrambling later?

Next up, I’ll translate what was “greenlit” into plain English and show the realistic ways Americans can use crypto for homebuying over the next 12 months.

What Fannie Mae actually “greenlit” (plain English, not hype)

When people hear “crypto-backed mortgages,” they picture some Wild West loan where you walk into a bank, flash a Ledger, and walk out with a 30-year fixed.

That’s not what’s happening.

What’s actually changing is much more boring (and that’s a good thing): Fannie Mae is signaling that verified crypto holdings can be recognized inside the mortgage underwriting framework under specific controls—things underwriters already understand like documentation, custody, ownership, valuation haircuts, reserve requirements, and re-verification close to closing.

In Fannie-land, “greenlit” doesn’t mean “anything goes.” It means something closer to:

- Crypto can be considered as a qualifying asset and/or collateral if it meets defined standards.

- Verification matters more than hype: who holds it, where it came from, and whether it can be valued and controlled reliably.

- Risk controls are the product: volatility buffers, conservative valuation, and clear paper trails.

So yeah, it’s big. But it’s big because it brings crypto into a system that only respects two things: proof and process.

Why this is a big deal: Fannie’s $4.3T scale changes lender behavior

Here’s the real reason this matters: mortgage lenders don’t just care whether they like an asset. They care whether they can sell the loan after they originate it.

Fannie Mae sits right in the middle of that machine:

- Originators (banks, brokers, credit unions) create the mortgage.

- Underwriters approve it based on what they believe will pass secondary-market standards.

- Fannie Mae (and the broader secondary market) influences what’s “acceptable,” which influences what lenders are willing to approve at scale.

So when Fannie starts acknowledging crypto under a defined rule set, it doesn’t just create one new loan product. It nudges the whole pipeline to stop treating crypto like it’s invisible.

Translation: lenders that previously said “sell it to cash or it doesn’t exist” suddenly have a reason to build a compliant workflow.

“Is this live policy or just talk?”

Smart question—because the mortgage world is full of headlines that hit your feed months before your local loan officer has the checkbox.

This is how I read the difference between “talk” and “real rollout”:

- Underwriting bulletins / lender overlays: banks publish internal guidance (often stricter than the baseline rule).

- Pilot programs: limited states, limited loan amounts, or “only if assets are held at X custodian.”

- Secondary-market acceptance: what matters is whether loans under these rules can be delivered cleanly without buyback risk.

If you’re trying to plan your next 12 months, here’s a realistic timeline I’d use:

- Next 3 months: more “crypto considered” applications appear via niche-friendly lenders and broker channels; lots of “case-by-case.”

- Next 6 months: clearer checklists emerge (custody, statements, wallet verification); more lenders quietly allow it with strict haircuts and reserve buffers.

- Next 12 months: broader availability—but still not universal. Expect “approved custodians,” conservative valuation, and very picky source-of-funds reviews.

One tip that saves time: when a lender says “Fannie-eligible,” ask a sharper question—“Is it eligible under your overlays, and have you closed one yet?”

How Americans can use crypto to buy a house in the next 12 months (realistic paths)

In 2026, I’m seeing three practical ways crypto fits into a home purchase. Each one has a different risk profile, and if you pick the wrong one you can create a mess right before closing.

Path A: Crypto counted as a qualifying asset (without selling)

This is the cleanest path for most people because it doesn’t require you to borrow against your crypto or trigger a taxable sale.

Think of it like this: if underwriting can verify you hold meaningful assets, that can help with:

- Reserves (months of payments available after closing)

- Overall borrower strength in borderline approvals

- Compensating factors when something else is tight (depending on the lender)

Real sample: Let’s say you’re buying a $550,000 home and your cash reserves are light after down payment and closing costs. But you’ve got $120,000 in BTC held with a mainstream custodian, clean history, and stable income. A lender might not count the full $120k at face value (haircut), but even a discounted value can materially strengthen your “reserves” story.

Why lenders like this: it’s closer to traditional underwriting logic—“verified assets reduce default risk.”

Path B: Crypto-backed loan first, mortgage second (bridge strategy)

This is the strategy people already use today: borrow against crypto to raise cash for down payment/closing, then apply for a traditional mortgage.

It can work, but it’s the path that bites people the most because it mixes two timelines:

- crypto market volatility (can move in a weekend)

- mortgage underwriting timelines (move in weeks)

Real sample: You borrow $80,000 against your BTC to fund a down payment. If BTC drops hard and your crypto loan has a liquidation threshold, you can get forced to add collateral or repay at the exact time you’re trying to satisfy mortgage conditions.

What the data says (why lenders worry): crypto’s volatility is structurally higher than traditional reserve assets. Studies from institutions like the Bank for International Settlements (BIS) and academic volatility research repeatedly show crypto experiences sharper drawdowns and clustering volatility than major FX pairs and broad equity indexes—exactly the kind of behavior that causes margin pressure at the worst time.

If you use this path, you need a plan for a sudden 20–40% drawdown. Not “hope.” A plan.

Path C: Use crypto as collateral inside the mortgage structure (the new headline)

This is the “crypto-backed mortgage” headline people are reacting to.

In mortgage terms, “collateral” is usually the house. Adding crypto as collateral means the lender may treat a portion of your crypto as pledged support for the loan—but under conservative constraints.

Here’s what I expect lenders to do (because it’s how they manage anything volatile):

- Haircut the value (e.g., count $100k BTC as $50–$70k for safety)

- Require overcollateralization (pledge more than the amount it’s supporting)

- Cap crypto’s share (limit how much of the collateral package can be crypto)

- Re-verify near closing (because a pre-approval from 30 days ago means nothing if BTC moved)

Plain-English takeaway: if you’re hoping to finance 95% of a home because you have crypto, don’t assume that’s how this will work. Early products will likely reward conservative borrowers—not maximize leverage.

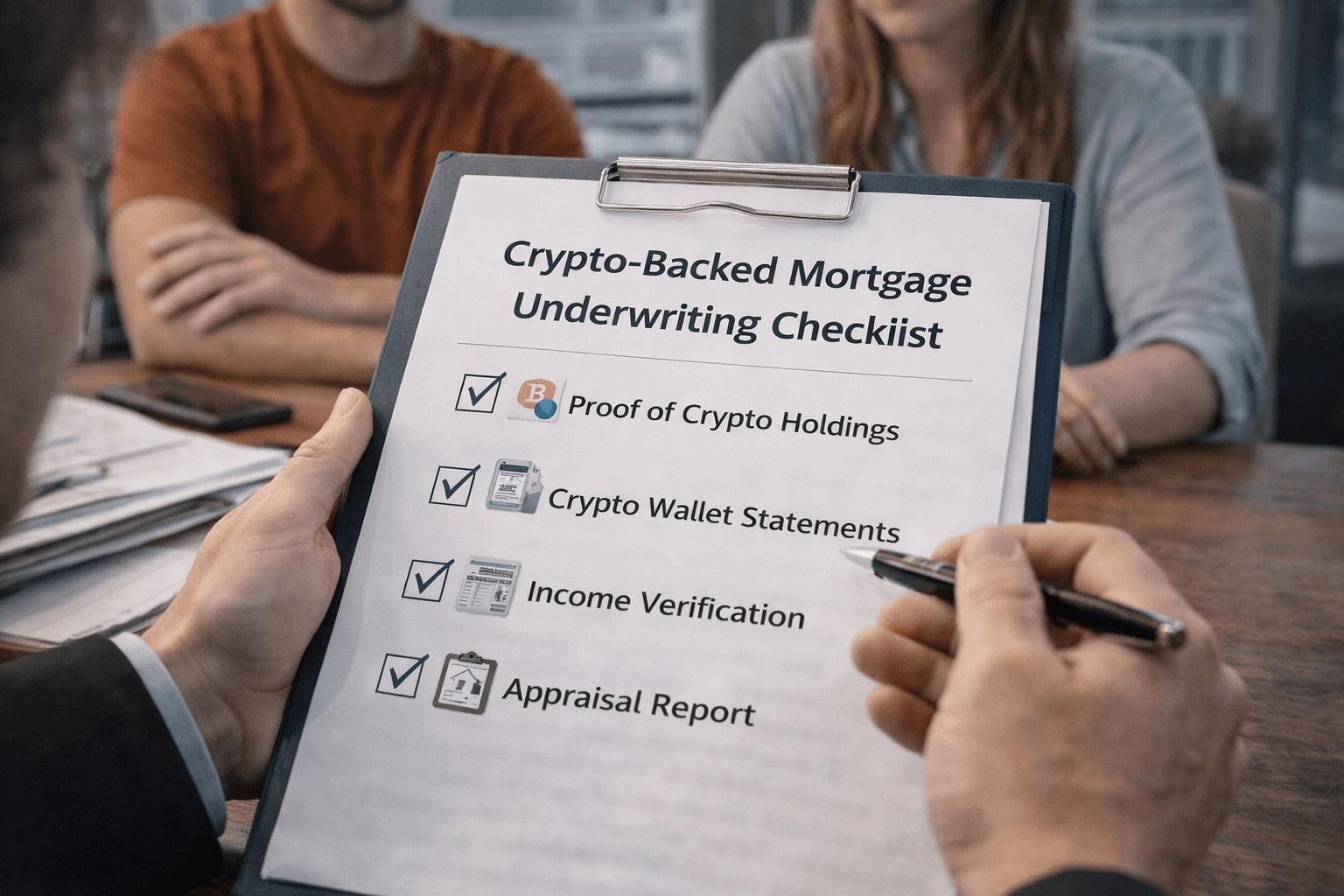

The underwriting checklist: what lenders will likely require from crypto holders

If you want your crypto to help you get approved, your job is to make an underwriter feel like they can prove three things:

- Ownership: it’s yours

- Source of funds: it came from understandable, documentable activity

- Control & accessibility: you can actually access it, and it isn’t tied up in weird restrictions

What usually won’t work on its own:

- random screenshots of a wallet balance

- a single exchange app screen with no identifying info

- “trust me, I mined it years ago” without supporting records

What tends to work better:

- exchange/custodian statements showing name, balances, and history

- tax documents (where applicable) tying activity to you

- wallet proof that you control the address (signing a message)

- transaction history exports that clearly show flow of funds

Custody rules: self-custody vs exchange vs ETF

If you want the smoothest underwriting, you want the most “bank-legible” custody possible.

- Easiest: regulated products like spot crypto ETFs (clear statements, familiar reporting)

- Often manageable: major exchanges / regulated custodians with strong reporting

- Most questions: self-custody, DeFi, cross-chain bridges, or assets touched by mixers

This isn’t me being anti-self-custody. I’m just telling you how underwriters think. They want a trail they can audit without guessing.

Quick reality check: if your coins hopped through five wallets, a bridge, and a privacy tool, you might still be totally legitimate—yet you’ve basically volunteered yourself for the slow lane.

Proof-of-ownership and transaction history (what “clean” looks like)

“Clean” doesn’t mean “never moved.” It means understandable.

What clean usually looks like:

- assets bought on a reputable platform

- withdrawal to one or two wallets you control

- clear deposits that match your income timeline and tax reporting

What slows files down:

- large inbound transfers from unknown addresses

- activity that resembles layering (even if it wasn’t criminal)

- “friend sent me six figures” with no documentation

Why lenders are strict here: compliance. On-chain analytics tools have become standard in risk teams, and public reporting (including research frequently referenced by firms like Chainalysis) has shown that while illicit crypto activity is a small share of total volume, it’s still a major compliance focus for banks because the reputational and regulatory costs are huge. Underwriters don’t want to be the person who approved the problem file.

Volatility controls: haircuts, LTV adjustments, and “what if BTC drops 30%?”

Every crypto-friendly mortgage conversation eventually hits the same wall:

“Okay, but what happens if Bitcoin drops 30%?”

Here’s what I expect lenders to do (and what I’m already hearing in the market):

- Haircuts: they’ll count less than market value toward qualification

- Higher reserve targets: “show me more months of payments available”

- Last-minute verification: re-check balances close to closing

- Conversion requests: in some cases, require part of reserves in cash or cash-like assets

Real sample: If you need $100,000 of “reserves,” a lender might accept $160,000 of BTC (haircut to 60–70%) instead of $100,000 of BTC at full value. It feels unfair until you remember: they’re underwriting a 30-year promise against an asset that can swing 10% in a day.

The questions everyone is asking

“Can I use Bitcoin to buy a house without selling it?”

In 2026, sometimes, yes—but only if you’re using a lender/product that can verify your BTC cleanly and apply volatility buffers.

Practically, this usually shows up as:

- BTC helping you qualify through reserves/asset strength (no sale)

- BTC supporting a collateral structure with haircuts and caps (limited, strict)

- a BTC-backed loan used carefully as a bridge (higher risk)

If you want “no sale,” your two best friends are clean custody and clean history.

“Which cryptocurrencies will qualify — only Bitcoin?”

Expect lenders to be conservative at first.

- Most likely: Bitcoin

- Possible: ETH (especially if held in simple custody, not wrapped/staked/levered)

- Most acceptable format: regulated products like spot ETFs (easy statements, familiar controls)

- Least likely: thin-liquidity altcoins, memecoins, anything hard to price or easy to manipulate

Even if a coin is “big on crypto Twitter,” that doesn’t mean an underwriting desk will touch it.

“Will using crypto change my mortgage rate or down payment?”

It can, but not in the way people hope.

- Rate: if the lender views the structure as higher operational/volatility risk, they may price it with a premium.

- Down payment: crypto doesn’t magically erase down payment rules; it may help you qualify by strengthening reserves or covering gaps through allowed structures.

One subtle win: stronger verified reserves can help approval odds even if your rate doesn’t drop. Approval is the real bottleneck for many buyers.

“How does this affect first-time homebuyers?”

This helps first-time buyers most when they have:

- solid income but limited cash reserves after closing

- meaningful crypto holdings with clean history

- a need to look stronger on paper without triggering a taxable sale

What it doesn’t change: income still matters, and DTI still matters. Crypto can support your file, but it usually won’t replace the basics.

“Is this safe? What are the risks I’m taking?”

It can be safe if you stay conservative. The big risks I watch for:

- Liquidation risk (if you borrow against crypto as a bridge)

- Custody risk (platform risk, account restrictions, operational hiccups)

- Regulatory/processing risk (a lender that says “yes” today can add overlays tomorrow)

- Tax/reporting risk (selling or moving assets at the wrong time can create ugly surprises)

Taxes, reporting, and the part people forget until it hurts

Here’s the simplest way to think about it:

- Selling crypto can trigger capital gains (or losses).

- Borrowing against crypto typically doesn’t trigger capital gains by itself, but you still pay interest/fees and take liquidation risk.

- Moving crypto around can create documentation headaches even if it’s not taxable—because underwriters may still want the story.

If you’re preparing for a mortgage file, treat your crypto history like it’s going to be audited. Because functionally… it is.

A simple “talk to your CPA” checklist before you do anything

If I were walking into a CPA meeting before a crypto-involved home purchase, I’d bring:

- Cost basis and holding periods (especially for any lots you might sell)

- Exchange tax forms (1099s if issued) and annual statements

- Wallet history exports (CSV where possible)

- Loan term sheets if you’re considering borrowing against crypto

- A “what if” plan: what happens if BTC drops 25–40% mid-process?

That last one matters more than people admit. Stress-testing isn’t paranoia—it’s how you avoid getting forced into a taxable sale at the worst possible moment.

Where I’m seeing the story reported (and why that matters)

I’m watching how this is being framed across mainstream finance and crypto-first outlets, because the tone tells you what phase we’re in: early interpretation, early pilots, or real lender rollout.

Here are the threads/posts I’m using to cross-check what’s being claimed (and how it’s spreading):

- WSJ on X

- Watcher.Guru on X

- Bloomberg Business on X

- CNBC on X

- Yahoo Finance on X

- BlockNews on X

- Crypto Curb on X

Why does this matter? Because when the story jumps from crypto media to mainstream business desks, it pressures lenders to respond—either with a product, or with a clear “not yet.” And that’s where the real opportunity is if you’re preparing early.

So here’s the question I want you to think about before you read what I’ll share next: if you had to buy a home within the next 12 months and BTC dropped 30% halfway through underwriting, would your plan survive—or would you be forced into a bad sale or a bad loan?

My take: what this means for the housing market and crypto in 2026

This is one of those shifts that doesn’t feel “real” until you see it change behavior in boring places: underwriting desks, risk committees, and the mortgage broker who used to tell you “crypto doesn’t count.”

When a system as big as Fannie Mae starts treating verified crypto as something it can understand and model, crypto becomes bank-legible. Not “cool.” Not “edgy.” Just… acceptable in spreadsheets.

And once that happens, a few things tend to follow:

- Mortgage lenders compete on who can approve more clean, well-documented crypto holders without taking scary risk.

- Homebuyers with crypto get optionality: you’re not forced into the “sell → pay taxes → wire cash → pray the underwriter likes it” path.

- Guardrails tighten to prevent ugly leverage loops (borrow against crypto to buy a house, then borrow against the house to buy more crypto…). The system will tolerate crypto—just not chaos.

On the housing side, don’t expect a magic “prices to the moon” button. Housing is local and supply still matters more than headlines. But I do think we’ll see micro-pressure in specific markets where:

- there’s already a high concentration of crypto wealth (think tech-heavy metros),

- inventory is tight, and

- buyers can move fast because their assets are recognized instead of ignored.

A real-world sample: imagine two buyers bidding on the same $650k home. Both have similar incomes. One has $220k in verified liquid assets in traditional accounts. The other has $220k in BTC/ETH held with a regulated custodian and clean history. In 2025, the crypto buyer often had to convert early, season funds, and deal with extra friction. In 2026, that friction drops—so the crypto buyer can make a cleaner offer with fewer “financing might be weird” vibes.

That “speed + confidence” effect is what moves markets at the margin.

Also, zooming out: studies keep showing the same theme—wealthy households are more likely to own crypto, and ownership rises with income and net worth. The Federal Reserve’s Survey of Household Economics and Decisionmaking (SHED) has repeatedly found crypto ownership is concentrated among higher-income groups (even as retail adoption has broadened). Translation: the buyers most capable of acting on this change are the ones who already tend to be competitive in housing.

That’s why I’m watching lenders’ risk controls closely. If the guardrails are sane (haircuts, conservative limits, strong verification), this becomes a “new lane” for qualified buyers—not a 2008-style free-for-all wearing orange laser eyes.

My base case: crypto doesn’t replace income in mortgage decisions—but it gets treated more like a real balance sheet asset, which helps approvals and reduces forced selling.

Who benefits most (and who should probably wait)

Not everyone should run at this. The winners are the boring ones—on purpose.

People who benefit most:

- Long-term holders with a simple story: bought over time, held, can document it.

- Buyers with steady W-2 or stable self-employment income where crypto is a strength, not the entire plan.

- Anyone with “clean” records: regulated exchanges/custodians, straightforward transfers, no mystery inflows.

- Conservative planners who can handle a drawdown without panicking or blowing up the deal.

People who should probably wait:

- Highly leveraged traders (if your net worth swings 40% in a month, mortgages and you are not best friends).

- Anyone depending on a bull run to qualify. If the plan is “BTC just needs to hit X and then I’ll be fine,” you’re gambling with your closing date.

- People with messy source-of-funds histories: cash deposits you can’t explain, coins that passed through mixers, random inbound transfers from unknown wallets.

- Buyers with tight cash flow where one volatility event could wipe out reserves and spook underwriting right before closing.

Here’s a simple gut-check I’d use if this were my own mortgage:

If Bitcoin dropped 30% next month, would I still qualify, still sleep, and still close without begging for exceptions?

If the honest answer is “no,” I’d slow down and build more buffer first.

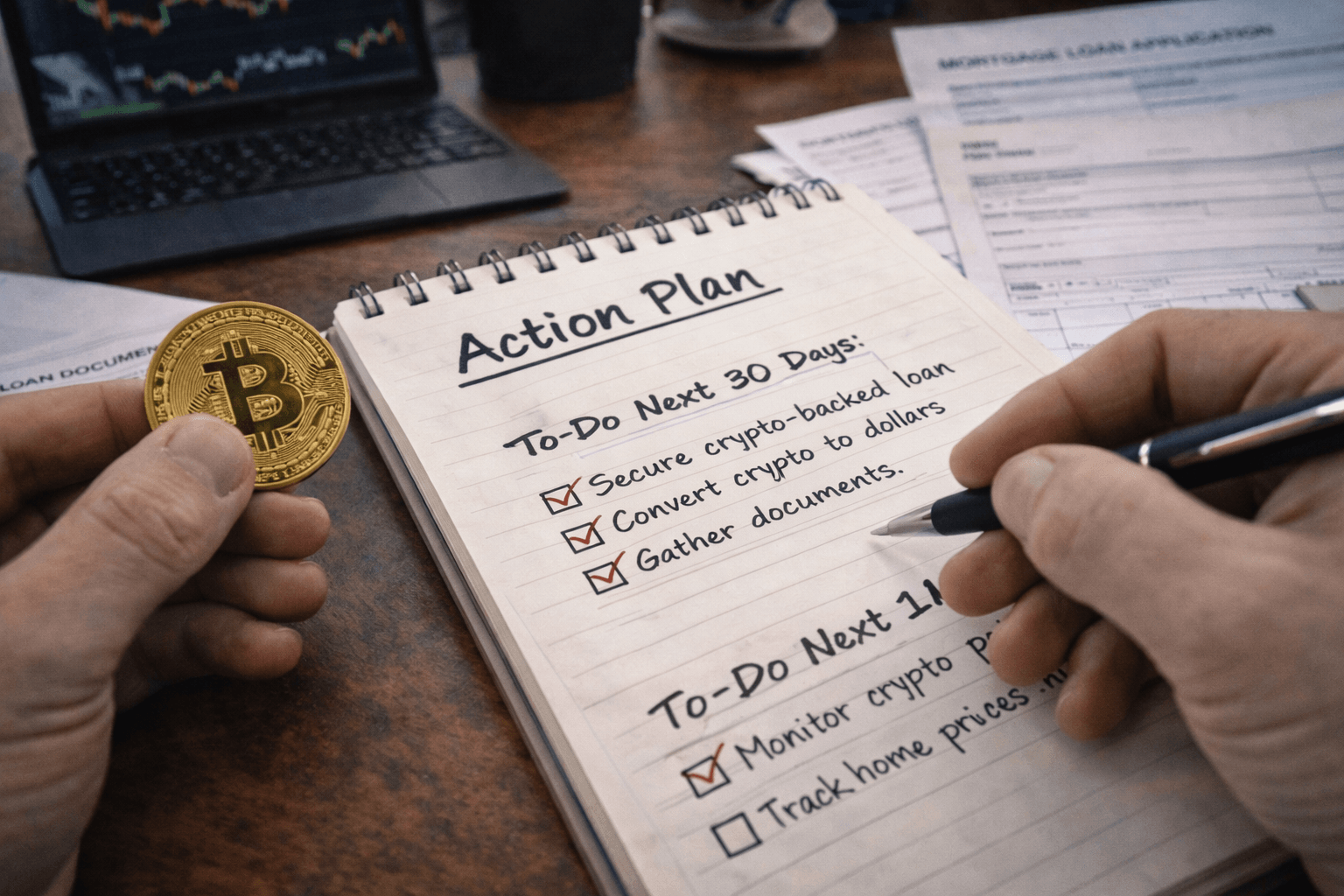

Your 30-day and 12-month action plan if you want to buy with crypto

If you’re serious about buying a home with crypto involved, your biggest advantage is preparation. Underwriting loves boring, documented, repeatable. So give it that.

What I would do in the next 30 days

- Clean up your paper trail (before you need it).

Download statements from exchanges/custodians, export transaction histories, and make a simple timeline of big moves (“moved 1.2 BTC from Coinbase to Fidelity custody on Feb 2,” etc.). If you ever get asked “where did this come from?” you want an answer in 30 seconds. - Choose a custody strategy that an underwriter won’t hate.

If you want the smoothest path, lean toward regulated custodians or well-known exchanges with strong reporting. Self-custody can still work in some cases, but it tends to create extra steps and questions. You’re not trying to win a cypherpunk award—you’re trying to close. - Stop sketchy transfers.

This is not the month to “try a new bridge,” run funds through questionable services, or accept random wallet-to-wallet transfers because a friend “owes you.” Keep it clean and explainable. - Talk to a mortgage broker who actually gets this.

Not “my cousin knows a loan guy.” Ask directly: “Have you closed loans where crypto assets were part of qualification or reserves? What documentation did underwriting accept?” If they dodge, move on. - Run a stress test like a grown-up.

Make a simple sheet with three scenarios: BTC/ETH down 10%, down 30%, down 50%. Then ask: do I still have enough reserves? Do I still meet the lender’s comfort level? Would I need to sell at the worst time?

What I would build over the next 12 months

- Increase “boring” reserves.

Even if crypto is recognized, having some traditional reserves (cash, money market, T-bills) makes approvals smoother and reduces the chance that a drawdown turns into a closing crisis. - Lower your DTI if you can.

Pay down high-interest debt, avoid new monthly obligations, and keep your credit profile stable. The more traditional your file looks, the easier it is for crypto to be treated as a plus instead of a complication. - Plan taxes like you actually like money.

If you might sell some crypto later for a down payment or reserves, plan when and how to do it. Holding period matters. Realized gains matter. And a forced sale because of timing is usually the most expensive kind. - Watch lender rollouts like you’d watch rate cuts.

The practical difference in 2026 won’t just be “allowed vs not allowed.” It’ll be product terms, haircuts, caps, re-verification rules, and how strict each lender is. Treat it like shopping for the best deal, not chasing the loudest headline. - Get “mortgage ready” before you shop.

Pre-approval is nice. A clean, well-documented file is better. The goal is to be the buyer whose offer feels safe to accept—because the seller’s agent believes you’ll close.

If you want one practical example of how this preparation pays off: the buyer who can instantly provide a neat PDF folder—statements, transaction exports, a simple source-of-funds summary, and a conservative reserve plan—will get “yes” faster than the buyer who shows up with screenshots and a hope that the underwriter is into crypto that day.

A grounded way to think about all of this

This is a legit shift, but it’s not going to feel like a sci-fi moment where you walk in with a Ledger, tap the desk, and walk out with a mortgage approval.

It’s going to look a lot more boring than that:

- clean documentation,

- conservative leverage,

- clear custody and verification,

- and a plan that still works if crypto has a bad month.

If you get those pieces right in 2026, you’ll be ahead of the wave—while everyone else is still arguing online about whether it’s “real” instead of getting their finances ready to actually close.